RLUSD Put to the Test by Ripple for Actual Trade Settlements in Singapore's MAS Sandbox

Within the MAS BLOOM sandbox environment, Ripple conducts testing of RLUSD for programmable settlement of trades, demonstrating the potential for stablecoins to expand beyond simple payment functions into practical business applications.

Singapore's BLOOM initiative and Ripple's participation: A measured advancement toward stablecoin adoption

Through Project BLOOM (Borderless, Liquid, Open, Online, Multi-currency), Singapore has reinforced its standing as a premier destination for tokenized financial services.

The collaborative program assembles a diverse consortium of conventional banking institutions, financial technology companies and stablecoin issuers to assess the integration possibilities of digital settlement instruments into current financial systems.

Among the noteworthy collaborations within this pilot program is the partnership between Ripple and supply chain technology provider Unloq. The two organizations are investigating automated settlement mechanisms for trade transactions utilizing Ripple's forthcoming stablecoin, RLUSD, operating on the XRP Ledger infrastructure.

Though Ripple's participation might seem to represent regulatory approval from Singapore's financial authorities, the actual situation is considerably more nuanced. The RLUSD stablecoin is presently functioning within a sandbox testing environment, representing a structured experimental phase concentrated on particular technical use cases rather than constituting comprehensive regulatory authorization.

Understanding the difference between this controlled experimental validation and formal regulatory licensing is critical for properly evaluating the initiative's present boundaries and prospects for future development.

The specific focus of Ripple's testing program

Under the Monetary Authority of Singapore's (MAS) BLOOM initiative, Ripple's pilot program addresses a particular problem: the automation of international trade settlement through the use of programmable digital currency.

The experimental framework combines three fundamental components:

- RLUSD functioning as the settlement instrument

- XRP Ledger serving as the underlying transaction platform

- Unloq's SC+ platform acting as the operational layer for trade finance operations

The system goes beyond merely transferring funds between counterparties; it has been engineered to trigger payment releases automatically when predetermined commercial requirements are satisfied. These prerequisites might encompass shipment acknowledgment, document authentication or funding activation points.

The evaluation of RLUSD extends beyond its function as a mere payment instrument, examining its potential as an integral component of a conditional settlement framework incorporated directly into commercial trade operations.

Did you know? Conventional trade finance operations continue to depend substantially on physical paper documentation including bills of lading, which frequently require days or potentially weeks for complete processing. Systems utilizing programmable settlement technology seek to digitize and streamline these operational processes.

Understanding BLOOM: What it represents and what it does not

In October 2025, MAS introduced BLOOM as a platform for investigating how tokenized currency could enhance settlement mechanisms across international boundaries and between financial institutions.

The scope of this initiative reaches far beyond any individual organization. Participants include financial institutions like DBS and UOB, infrastructure companies such as Partior, and stablecoin providers including Circle. Ripple represents merely one contributor within this expansive collaborative network.

Crucially, BLOOM does not constitute an operational production platform. The initiative operates as a sandbox-style testing ground enabling organizations to evaluate financial innovations while maintaining regulatory supervision.

Consequently, participation within the program does not signify that MAS has granted approval for RLUSD to function as a widely recognized settlement instrument. Rather, it demonstrates that MAS considers the suggested application sufficiently worthwhile to examine within a monitored framework.

Acknowledging this important distinction prevents a frequently occurring misinterpretation. Engagement in a regulatory sandbox represents supervised testing and experimentation, rather than constituting formal regulatory validation or endorsement.

The complexity of trade finance as an evaluation scenario

Trade finance operations present significantly greater complexity compared to simple payment transactions. Typical transactions encompass numerous stakeholders, including exporters, importers, financial institutions, insurance companies and shipping providers, accompanied by multiple documentation layers and dependent contractual requirements.

Payment execution seldom occurs instantaneously. Instead, payments remain linked to particular triggering events, including:

- Confirmation of shipment departure

- Validation of delivery completion

- Authentication of required documentation

- Achievement of credit approval or financing benchmarks

Conventional systems address these interdependent requirements through manual processing and intermediary involvement, frequently producing delays, processing mistakes and insufficient visibility.

Through its RLUSD pilot program, Ripple attempts to resolve this operational complexity by incorporating payment execution logic directly within the settlement infrastructure. Rather than processing documentation independently before authorizing payments, the entire process occurs within a singular, integrated operational framework.

This methodology differentiates the pilot from the majority of stablecoin implementations. The focus extends well beyond simply accelerating monetary transfers. Rather, it emphasizes the synchronization of monetary movement with actual commercial requirements occurring in real time.

Did you know? Initially, stablecoins gained widespread adoption primarily as liquidity instruments within cryptocurrency trading platforms, but financial regulators are progressively examining their potential applications in conventional financial systems, including international payment processing and settlement infrastructure.

The distinction between sandbox participation and regulatory authorization

Ripple's engagement in BLOOM occurs simultaneously with a distinct regulatory advancement. In December 2025, MAS broadened the spectrum of payment operations authorized under the Major Payment Institution (MPI) license maintained by Ripple's Singaporean subsidiary.

This modification to the licensing framework enables Ripple to provide an expanded portfolio of regulated payment solutions within Singapore.

However, the BLOOM pilot program remains a separate matter. The initiative does not seek to authorize Ripple's products for general commercial deployment, but instead aims to determine whether a particular settlement framework operates efficiently under practical conditions.

The differentiation can be articulated as follows:

- MPI license expansion: Official regulatory permission for expanded payment service offerings

- BLOOM pilot: Supervised evaluation of programmable settlement technology

Conflating these separate developments could lead to overstating the regulatory importance of the pilot initiative. BLOOM has been structured to explore technical and practical operational questions, rather than to validate or promote any particular settlement approach over alternatives.

The wider tokenization framework in Singapore

Ripple's pilot program forms one component of an extensive MAS exploration into tokenized financial systems across various sectors.

In November 2025, MAS revealed intentions to distribute tokenized MAS bills to primary dealers, with transaction settlement enabled through a wholesale central bank digital currency (CBDC). During approximately the same period, the authority also updated its regulatory guidance concerning tokenized capital market instruments to establish clearer regulatory parameters.

These developments indicate a comprehensive strategy. Rather than exclusively promoting one particular form of digital currency, Singapore is evaluating a diversified settlement ecosystem incorporating:

- Tokenized liabilities issued by banks

- Regulated stablecoin products

- Wholesale central bank digital currencies

- Tokenized security instruments

Within this comprehensive testing framework, RLUSD constitutes one potential settlement vehicle among multiple alternatives.

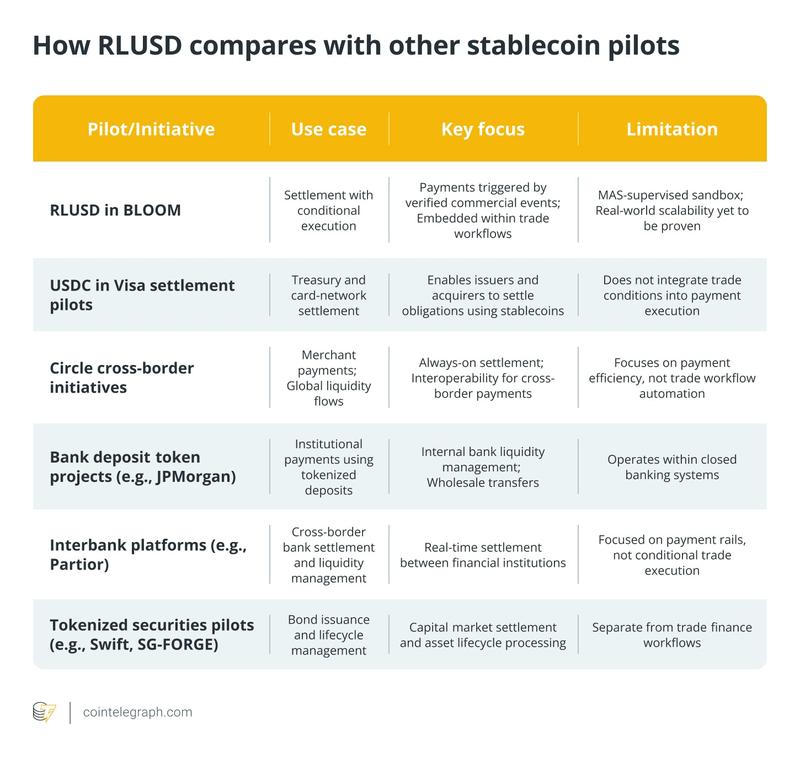

Comparative analysis of RLUSD against other stablecoin pilot programs

Ripple's methodology diverges from alternative stablecoin and tokenized currency trials currently in progress across multiple significant dimensions:

Distinguishing characteristics of the RLUSD pilot initiative

Three primary characteristics set Ripple's pilot program apart: the incorporation of conditional settlement mechanisms, the integration with commercial trade processes and operation within a multi-asset framework.

- Conditional settlement logic: In contrast to the majority of stablecoin pilot projects, RLUSD undergoes testing within a framework where payment execution depends upon actual real-world events. This introduces a dimension of programmability that significantly exceeds basic value transfer operations.

- Integration with trade workflows: The pilot program incorporates settlement capabilities directly within trade finance operational processes rather than handling it as an independent function. This integration potentially minimizes fragmentation across documentation handling, financing arrangements and payment execution.

- Multi-asset environment: RLUSD receives evaluation alongside tokenized banking liabilities. This approach aligns with MAS' overarching goal of establishing interoperable settlement instruments rather than depending upon a single predominant model.

When considered together, these characteristics position RLUSD within a more comprehensive investigation into programmable financial systems rather than confining it exclusively to digital payment applications.

Notwithstanding its promise, the pilot program leaves multiple significant questions requiring resolution:

- Is it feasible to reliably digitize and authenticate trade conditions in real time?

- Will smaller commercial enterprises genuinely gain improved access to financing opportunities?

- Can stablecoins and bank-issued tokens operate concurrently without creating liquidity fragmentation?

- How will regulatory frameworks adapt if these systems progress beyond experimental stages?

These outstanding questions emphasize that the pilot does not represent a comprehensive solution. Instead, it constitutes an investigation into whether an alternative settlement architecture can operate efficiently when deployed at scale.

Did you know? Smart contract technology can minimize settlement risk through ensuring that monetary transfers occur exclusively when predefined requirements have been fulfilled. This capability can help decrease disagreements resulting from inconsistent documentation in cross-border trade transactions.

Consequences for stablecoin development and settlement architecture

The BLOOM initiative indicates that the evolution of digital settlement infrastructure may not be characterized by dominance of any singular asset category or technological platform.

Rather, regulatory bodies such as MAS appear to be evaluating a stratified methodology wherein various forms of tokenized currency fulfill different functional roles:

- Stablecoins providing programmability capabilities and cross-platform compatibility

- Bank-issued tokens delivering institutional liquidity

- Central bank digital currencies ensuring sovereign settlement guarantees

Ripple's RLUSD pilot program contributes to this continuing experimentation, presenting one viable framework for how stablecoins might expand beyond straightforward payment applications into more advanced financial operational processes.