Can Bitcoin Reach $115K by Year-End? Analyzing the Options Market Data

Options market data reveals bullish traders eyeing a $115,000 Bitcoin price target by December's close, but is this optimism grounded in reality?

Key takeaways:

- Approximately half of the $6 billion Bitcoin options open interest represents long-shot positions employed for hedging purposes and strategies that remain neutral to price movements.

- Professional market participants appear concerned about downside risk, as evidenced by the 9% premium on put (sell) options.

Bitcoin (BTC) enthusiasts are placing significant bets on the year-end options expiration scheduled for Dec. 25, with approximately $6 billion in total stakes. The cryptocurrency's impressive 33% rally from its Feb. 6 yearly bottom of $60,130 has rekindled optimistic sentiment among market participants. Yet, the substantial volume of call (buy) options positioned at $115,000 and beyond for the Dec. 25 expiry prompts examination of whether market optimism has reached excessive levels.

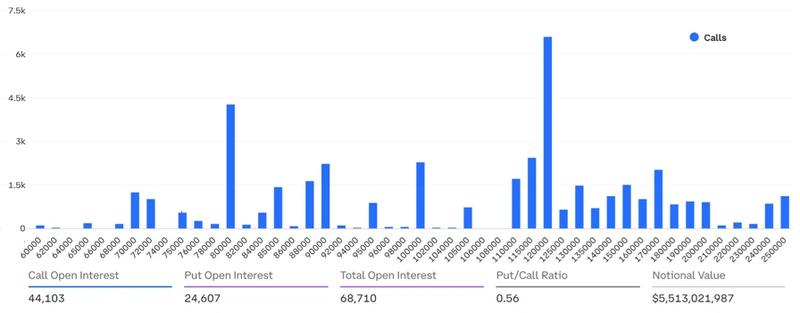

With a commanding 92% market share in December Bitcoin options open interest, Deribit exchange accounts for $5.5 billion of the total. Nevertheless, the true value upon expiration will likely be considerably reduced. A significant portion of these derivative contracts were established on low-probability scenarios, functioning as protective hedges or as components of neutral trading strategies designed to generate profits without requiring substantial price movements.

Call options lead the market, yet unrealistic positions exist on both sides

On Deribit, put (sell) options represent 56% less volume when compared to call options. The cryptocurrency trading community typically maintains a bullish bias, which naturally creates an imbalanced put-to-call ratio. Nevertheless, the $1.85 billion in open interest concentrated in call options at strike prices of $115,000 and above demands attention. This concentration warrants a detailed examination of how the optimistic call option positioning compares against the bearish puts.

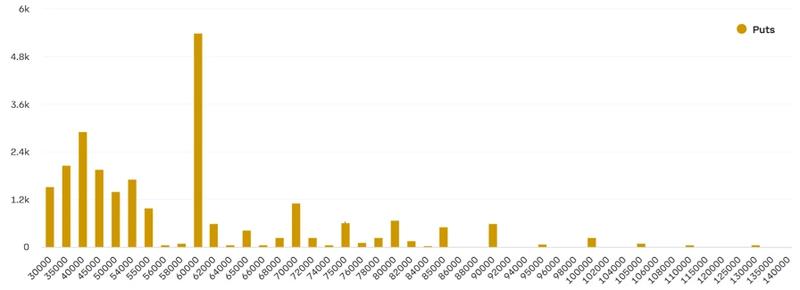

Equally remarkable is the substantial concentration of put options positioned at $55,000 and below, representing $1 billion in combined open interest. This distribution reveals that the proportion of positions deemed unlikely to materialize is comparable across both camps, accounting for approximately 50% of open interest in each category. When bulls face accusations of excessive optimism, the bears demonstrate equally extreme negative sentiment.

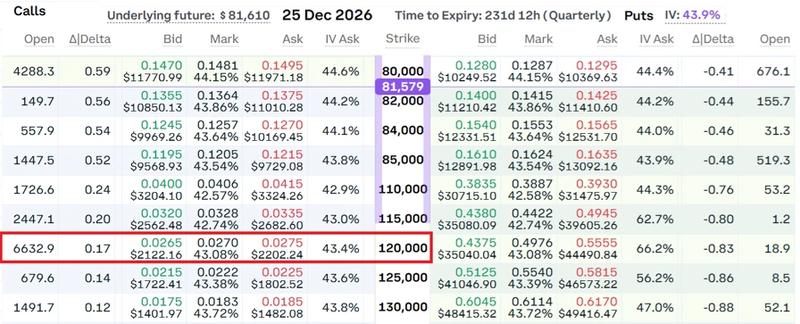

Apart from functioning as offsetting positions in multi-legged strategies with varying expiration dates, a $120,000 strike call option provides economical access to extreme bullish scenarios. According to May 7 pricing data from Deribit, traders pay $2,202 to acquire unlimited profit potential on the equivalent of one complete Bitcoin at prices reaching $120,000 or higher on the Dec. 25 expiration date.

The options skew indicator delivers a more precise assessment of how professional market participants perceive the probability and magnitude of both upward and downward price movements.

Currently, put options command a 9% premium when compared to calls with equivalent characteristics, indicating moderate apprehension regarding potential Bitcoin price declines. In balanced market conditions, this skew measurement typically fluctuates within a range of -6% to +6%. Based on derivatives market data, the recent surge to $80,000 failed to significantly boost investor confidence.

In conclusion, the $1.85 billion concentrated in December call options positioned at elevated strike prices should not be viewed as evidence of unreasonable bullish overconfidence.