Bank of England shows growing acceptance of stablecoins while criticizing insufficient industry engagement

The UK's central bank demonstrates willingness to adjust its stablecoin regulatory proposal, though a senior official has expressed disappointment over the quality of feedback received from the cryptocurrency sector.

The stance of the Bank of England (BOE) regarding stablecoins has been shifting toward a more accommodating position, though the institution's deputy governor has expressed concerns that meaningful dialogue with industry stakeholders remains insufficient.

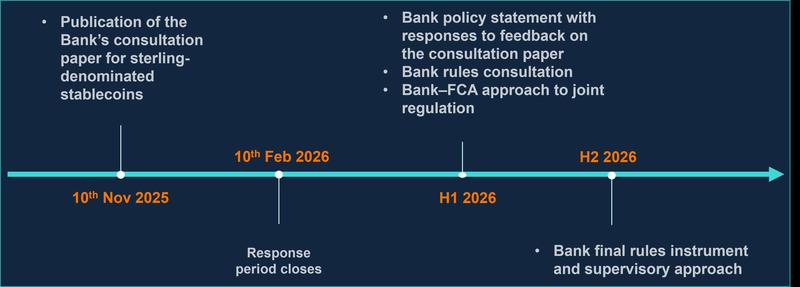

The central bank of the United Kingdom initiated a public consultation on stablecoins in November of last year. Certain requirements outlined in the proposal sparked criticism from cryptocurrency sector representatives, with complaints that such measures could hamper innovation.

During recent months, the institution has engaged with various industry organizations to refine its approach to stablecoins. This engagement has included reconsidering reserve backing requirements and reevaluating proposed account limitations.

Certain industry analysts suggest that the institution is demonstrating increased receptiveness toward stablecoins, though significant challenges remain to be addressed.

Bank of England open to feedback on stablecoin risk

On Nov. 10, 2025, the BOE published a document detailing its framework for regulating stablecoins. This followed two years after an initial discussion paper that, as stated by the bank, incorporated viewpoints from "banks, non-bank payment service providers, payment system operators, trade associations, academia, and individuals."

During that period, industry experts informed Cointelegraph that BOE was exaggerating the potential risks stablecoins could present to the United Kingdom's economy. Tom Rhodes, chief legal officer at UK-based stablecoin issuer Agant, remarked at the time that the institution was being "disproportionately cautious and restrictive."

Among the more contentious proposals were limits on stablecoin holdings, specifically 20,000 pounds for individuals and 10 million pounds for businesses that accept it as a form of payment.

Currently, signs indicate that the institution is reconsidering its position. During testimony before the House of Lords Financial Services Regulation Committee on Wednesday, BOE Deputy Governor Sarah Breeden informed MPs that the bank is willing to reconsider those limitations.

According to Breeden, the suggested limitations were intended to address concerns about a substantial migration of deposits toward stablecoins, which could potentially undermine banking stability.

"We proposed holding limits as a way of managing that risk. We are open to feedback on other ways of achieving it," she said.

Nevertheless, the quality of feedback has emerged as a concern, at least from Breeden's perspective. She stated, "The pressure from the industry to do it in a different way is very real. What we've been a bit disappointed with, is nobody said, 'Why not do it this way?'"

"I don't think we've yet had constructive engagement on a different way to solve the problem that I might have hoped for. Instead, what we've had is 'don't do this,' and 'I understand why you want to do something' as opposed to filling the gap."

Speaking to Cointelegraph on Thursday, Rhodes disputed this characterization. "Over the past two years we have reviewed thousands of pages of consultations from the FCA and the Bank, attended numerous roundtable meetings, and submitted hundreds of pages of input both ourselves and as part of trade associations."

According to Rhodes, the primary difficulty for both industry participants and regulators stems from the fact that they are developing a "comprehensive regulatory regime for a market that has yet to develop."

Rhodes explained:

"It's not possible to provide concrete data in the circumstances, which is why lighter touch principles-based regimes are appropriate at this nascent stage."

Nick Jones, the founder and CEO of UK-based digital assets platform Zumo, stated, "Industry groups have been working hard, and to tight deadlines, to make tangible recommendations."

According to Jones, the feedback process could become more productive if the institution adopted the Financial Conduct Authority's (FCA) Spring model. These time-boxed workshops focus on practical applications of the technology to answer regulators' questions.

The 'multi-moneyverse' and what's next for stablecoins in the UK

In her opening statements, Breeden provided reassurance that within the institution, "we do want to see tokenized money issued by non-banks."

"We can have what I call a 'multi-moneyverse' with greater choice and competition today."

This type of framework, as she described in a September speech, is "characterised by choice across different forms of money and payment; with technology driving faster, cheaper, and more innovative payments for the benefit of business, households, and users of financial markets; and — critically — with the whole system underpinned by trust in money itself."

Competition between different forms of money and its claimed advantages have long been central arguments advanced by the cryptocurrency sector. According to Rhodes, "Stablecoins being part of a competitive multi-moneyverse represents a substantial and positive evolution in the Bank's thinking."

Rhodes observed, however, that this position stood in "sharp contrast" to BOE Governor Andrew Bailey's statements, where "he doesn't see stablecoins as a substitute for commercial bank money."

According to Jones, "Over time, we've seen the Bank of England's scepticism towards digital assets start to dissipate." He finds it "encouraging" that the central bank has become more open to competing monetary forms and that pound sterling-backed stablecoins can coexist with fiat money.

"It's clear that different emerging types will fit different use cases — for example, large institutional capital is more comfortable with tokenised deposits while smaller retail payments companies can tap into the network effect of stablecoins," he said.

According to Rhodes, the subsequent stage involves a definitive policy statement from the BOE, though modifications remain possible.

Industry participants continue advocating for the elimination of holding caps and the removal of bank-style capital requirements for issuers. According to Jones, the latter "are inappropriate for fully-backed issuers, and should be replaced with oversight focused on reserve quality and transparency."

Another priority for the industry is reconsidering reserve requirements. Currently, BOE mandates that issuers maintain 40% of reserve assets in unremunerated Bank of England deposits and up to 60% in high-quality, short-term UK government debt.

This framework draws from previous failures such as the Silicon Valley Bank collapse in 2023 that caused the USDC stablecoin to lose its peg. Speaking to Reuters, Breeden stated, "Those numbers are broadly in line with that. That's why we're proposing 40% rather than a smaller number."

"Regulators should perhaps consider remunerating a portion of the 40% held at the Bank of England to help maintain commercial viability," said Jones.

"The UK can be one of the leaders in stablecoins, but only if regulation is proportionate and competitive."