Mastercard's Strategy to Process Card Transactions Using Stablecoin Technology

The payment giant Mastercard has begun trials for settling card transactions using SoFiUSD stablecoin, a move designed to accelerate clearing processes and connect conventional banking with blockchain technology.

Key takeaways

- Mastercard is bringing stablecoins into its payment processing framework to enhance the settlement infrastructure on the back end, giving financial institutions and card issuers the ability to clear transactions using regulated digital currencies like SoFiUSD.

- Through its collaboration with SoFi Technologies, SoFi Bank gains the capability to process Mastercard transactions using SoFiUSD, while the Galileo platform extends stablecoin settlement options to additional financial institutions and fintech card issuers.

- The stablecoin settlement approach targets the clearing phase that happens after transactions are completed, which means everyday cardholders will experience no changes in how they use their cards, even though the settlement between financial institutions may happen via blockchain-powered digital currencies.

- Using its Multi-Token Network (MTN) infrastructure, Mastercard intends to accommodate various types of tokenized currency, including stablecoins, tokenized bank deposits and digital versions of traditional fiat money.

Digital stablecoins are progressively breaking free from their crypto-only origins and entering conventional financial conversations. Mastercard's decision to incorporate stablecoins into its card payment settlement operations serves as a clear illustration. Instead of discarding the existing card payment framework, Mastercard is enhancing the technological infrastructure behind the scenes by incorporating regulated digital dollar instruments into the process.

Through its collaboration with SoFi Technologies, this payments industry leader is experimenting with ways these blockchain-based assets can improve transaction settlement efficiency throughout its extensive network. This development demonstrates that the planet's most significant payment processing systems are getting ready for an era where conventional banking practices and digital currency technologies operate in tandem.

The SoFiUSD partnership

Mastercard's latest program centers around a collaborative effort with SoFi Technologies, which has launched a stablecoin backed by US dollars known as SoFiUSD.

According to this agreement, SoFi Bank, N.A. plans to utilize SoFiUSD for settling its Mastercard-branded credit and debit card payments. At the same time, SoFi's payment processing platform, Galileo Financial Technologies, will provide banks and fintech companies using its infrastructure the option to choose stablecoin settlement via Mastercard's network.

SoFiUSD comes from a federally chartered financial institution in the United States and reportedly operates with a 1:1 cash backing model, making it more similar to digitized bank money than to traditional cryptocurrency assets.

Did you know? The first credit card to gain wide acceptance across multiple merchants was launched by Diners Club in 1950. Cardholders originally received paper statements and paid their bills monthly, laying the foundation for today's global card payment networks.

Understanding card settlement

Mastercard's methodology becomes clearer when you grasp the typical mechanics of card payment processing. When someone uses their card by tapping or swiping it, these stages occur:

- The payment is authorized.

- The transaction is recorded.

- The merchant receives confirmation.

- The issuing and acquiring banks complete settlement at a later stage.

This ultimate settlement stage customarily happens through standard banking infrastructure during scheduled clearing periods.

Mastercard's stablecoin approach focuses exclusively on this backend settlement operation. It doesn't alter the way users engage with or start payments. From the consumer's viewpoint, the checkout experience would stay exactly the same.

How stablecoin settlement would work

With stablecoin settlement capability, Mastercard's infrastructure would permit participating financial institutions and card issuers to fulfill transaction requirements using digital dollars instead of depending exclusively on conventional fiat currency transfers.

In operational terms, the workflow might proceed like this:

- A customer initiates a card payment in their local currency.

- Mastercard determines the settlement obligations between the issuing bank and the acquiring bank.

- Instead of relying only on conventional banking channels, one or both parties may settle using stablecoins such as SoFiUSD.

Since stablecoins function on blockchain technology, they provide the possibility for around-the-clock settlement that doesn't depend on standard banking operating hours.

This approach has the potential to minimize delays in international payments and simplify liquidity oversight for banking organizations.

Did you know? The term "stablecoin" became popular around 2014, but the concept of digital dollars backed by real-world assets had been explored even earlier through experimental crypto projects that attempted to maintain price stability using collateral and algorithmic mechanisms.

The role of Mastercard's multi-token network

The underlying infrastructure for this program is Mastercard's Multi-Token Network (MTN). This platform is engineered to accommodate several varieties of tokenized currency, such as:

- Stablecoins

- Tokenized bank deposits

- Representations of fiat currency

- Other digital assets

By connecting traditional banking infrastructure with blockchain-powered tokens, Mastercard aims to establish an adaptable settlement framework where regulated digital currencies can function alongside conventional financial systems.

The platform would give financial institutions the ability to move value with greater efficiency while maintaining adherence to existing regulatory requirements.

Why Mastercard is entering the stablecoin space

Stablecoins have emerged as among the most rapidly expanding segments of the cryptocurrency ecosystem in recent years. They merge the price consistency of traditional currencies with the velocity and operational advantages of blockchain infrastructure. Consequently, they can facilitate rapid transfers, programmable payments and almost instantaneous settlement throughout worldwide networks.

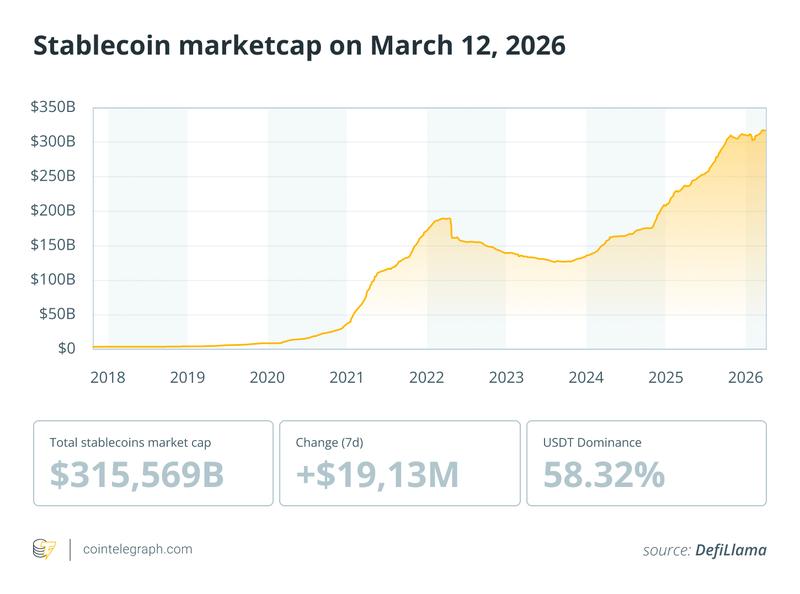

As of March 2026, the stablecoin market had reached a significant milestone, with its total valuation climbing to approximately $314 billion, according to DefiLlama data. This growth followed a breakout year in 2025, during which transaction volumes reached a record $969.9 billion in a single month. Experts now project that monthly volumes are on track to surpass the $1 trillion mark by the end of 2026.

For Mastercard, embedding stablecoins into its settlement framework helps guarantee the organization stays pivotal to the evolving digital payments landscape.

Instead of attempting to compete directly with blockchain platforms, Mastercard is establishing itself as a bridge linking conventional finance with digital currency ecosystems.

Expanding beyond simple payments

The strategic alliance between SoFi and Mastercard also aims to investigate supplementary financial use cases for stablecoins.

Potential uses include:

- Cross-border remittances

- Business-to-business payments

- Treasury management tools

- Stablecoin-linked card programs

Stablecoins might enable corporations to automate sophisticated financial processes through programmable transactions.

For example, businesses could automatically release payments when contractual conditions are met, reducing manual intervention and operational costs.

Competition from Visa

Mastercard is not alone among global card networks in exploring stablecoin integration. Its main competitor, Visa, has also expanded its use of digital currencies for payment settlement.

Visa has tested cross-border settlement using stablecoins such as USD Coin (USDC), allowing financial institutions to pre-fund international transfers with tokenized dollars. The company has also explored enabling businesses to send payouts directly to stablecoin wallets.

These initiatives indicate that stablecoins are becoming an essential component of the wider infrastructure rivalry among major payment processing networks.

Why regulation will be crucial

The integration of stablecoins into mainstream financial infrastructure relies significantly on regulatory frameworks.

Financial institutions need clear regulatory frameworks that address key concerns, including:

- Reserve backing

- Redemption guarantees

- Anti-Money Laundering (AML) compliance

- Operational resilience

Because SoFiUSD is issued by a regulated US bank, it is likely to inspire greater confidence among regulators and financial institutions than stablecoins that originate in the crypto space.

Payment networks such as Mastercard are therefore prioritizing regulated stablecoins issued by licensed institutions.

Challenges to widespread adoption

Despite growing interest, several challenges could limit the wider adoption of stablecoin settlement.

These challenges include:

- Integration complexity for banks and payment processors

- Regulatory differences across jurisdictions

- Liquidity management between fiat and digital assets

- Interoperability between blockchains and financial networks

Furthermore, everyday consumers probably won't perceive substantial differences since the technology primarily impacts backend systems rather than customer-facing payment interactions.

The bigger picture for digital payments

Mastercard's stablecoin initiative is part of a broader transformation taking place in global finance. Stablecoins were initially used mainly for cryptocurrency trading. Today, they are increasingly viewed as potential tools for payments, remittances and broader financial infrastructure.

If stablecoin settlement proves efficient and reliable, card networks could eventually operate within a hybrid system that combines traditional banking rails with blockchain-based digital assets.

Mastercard is not looking to replace traditional payments. Rather, it is upgrading the under-the-hood infrastructure of global card networks. By integrating regulated stablecoins like SoFiUSD into its Multi-Token Network, the company is preparing its infrastructure for a more digital economy.

The goal is to create a system that is faster, more flexible and available 24/7, while ensuring the average shopper notices no difference at the checkout counter.