Fragmented liquidity makes stablecoins mirror forex markets, warns Eco CEO

While stablecoins offer the promise of frictionless dollar transactions, liquidity fragmentation is creating complicated execution challenges for large-scale transfers, according to Eco CEO Ryne Saxe.

The stablecoin ecosystem functions like a fragmented foreign exchange marketplace, with liquidity dispersed across various blockchains and liquidity pools, resulting in price disparities and inconsistent access to dollar-denominated liquidity.

On the surface, transferring stablecoins appears straightforward. However, beneath that simplicity lies a frequently complex, multi-step process that gets routed through different chains and liquidity pools.

"It's a very special case of a foreign exchange market onchain, and that leads to bad user experience, with unexpected slippage, transaction reversion and unfamiliar information when moving your dollar from point A to point B," Ryne Saxe, CEO at stablecoin infrastructure company Eco, told Cointelegraph.

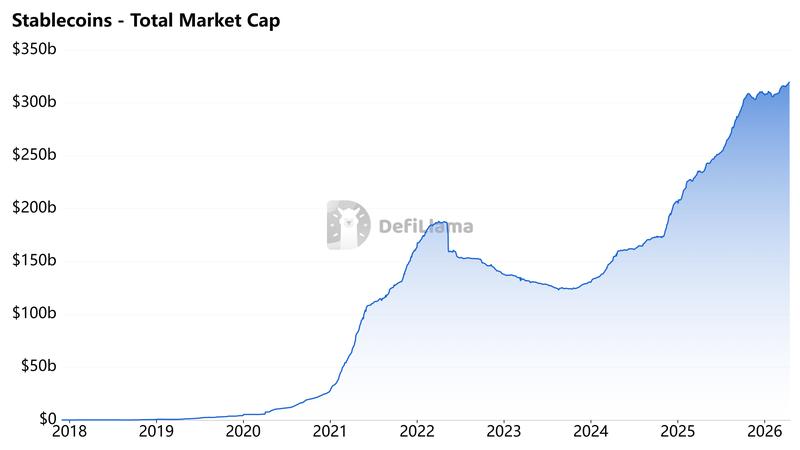

The stablecoin market has grown to exceed $320 billion in total market capitalization, with Tether's USDt (USDT) and Circle's USDC (USDC) commanding the largest shares.

However, as institutional players and high-volume traders increasingly participate in the ecosystem, executing large-scale stablecoin transfers cleanly has become progressively more challenging.

Stablecoins aren't as fungible as they seem

While a stablecoin might be pegged to the dollar — or alternative fiat currencies — it doesn't function as a unified asset in practice, with liquidity fragmented across different issuers, blockchain networks and decentralized finance (DeFi) platforms, each featuring distinct depth, pricing mechanisms and access requirements.

"Stablecoins, between them, aren't very fungible," said Saxe. "The different profiles between those markets mean pricing and moving stablecoins seamlessly and efficiently across them is actually a hard problem that people take for granted."

In real-world scenarios, a dollar-pegged stablecoin on a particular chain may not hold equivalent value to the identical asset on a different network. Variations in collateral backing structures, market accessibility and liquidity depth generate pricing discrepancies that expand with transaction size or in markets with lower liquidity.

These differences are generally minimal in highly liquid markets and for smaller-sized transactions. However, as transaction volumes increase, these gaps become substantially more pronounced.

"The more major DeFi markets focus on stablecoins, the more chains focus on stablecoins, the more stablecoin assets there are, the more fragmented," Saxe said. "People think these are just dollars, but they're actually not."

A March report published by payments startup Borderless revealed that price divergence in stablecoins is heavily influenced by the source of liquidity.

The analysis gathered hourly buy and sell pricing data throughout the month of February across 66 different stablecoin-to-fiat corridors — or conversion pathways such as USDC to Mexican pesos — encompassing 33 distinct currencies and seven separate blockchains. The findings demonstrated that USDC and USDT maintained nearly identical trading prices in the majority of instances.

More significant disparities surfaced at the individual provider level, where pricing spreads within the same corridor could surpass hundreds of basis points, resulting in execution quality that depends heavily on liquidity access and routing capabilities across different venues.

Stablecoins become harder to move at size

In their current configuration, the market structure of stablecoins mirrors foreign exchange systems, where dollar equivalents circulate throughout disconnected marketplaces, according to Saxe. This characteristic becomes increasingly apparent when executing larger stablecoin transfers across blockchain networks.

Stablecoins have emerged as a critical component for institutions entering the digital asset space, utilized for trading activities, cross-border payment solutions and onchain treasury management operations. Financial firms depend on these assets to transfer capital between platforms, settle transactions and access yield-generating opportunities throughout DeFi markets.

In contrast to retail participants, institutional entities frequently transfer tens of millions of dollars in single transactions, requiring execution that delivers speed, predictability and efficiency.

"If liquidity is spread out, trying to sell $10 million of one stablecoin and buy $10 million of another in a single step will move the market," Saxe said. "What usually needs to happen is breaking that transaction into multiple branches, which may route differently and converge at the destination."

Under these circumstances, fragmentation transforms into a significant limitation. Rather than accessing a unified pool of dollar liquidity, institutional participants must navigate across multiple chains, various issuers and diverse venues, each presenting different liquidity characteristics. Transferring substantial amounts can impact prices, necessitate trade splitting and introduce unpredictability into the execution process.

"Right now, they don't have the risk management, trust and infrastructure that they need to move or hold a lot of stablecoins at size onchain by default," Saxe said.

Stablecoins need infrastructure, not more supply

Various companies have begun developing infrastructure solutions to bridge these gaps, though they're approaching the challenge from differing perspectives regarding the fundamental nature of the problem.

Circle views stablecoins as the foundational layer of an emerging FX system, where multiple currencies, liquidity providers and settlement layers integrate through common infrastructure. In contrast, Eco concentrates on routing and execution capabilities, aggregating liquidity from fragmented market sources.

Both methodologies acknowledge the challenge that stablecoins operate across multiple chains or issuers, while the underlying liquidity remains distributed and uneven. Transferring funds necessitates engaging with this fragmented liquidity landscape, which introduces pricing variations, routing complications and execution uncertainty.

"Fragmentation creates more spread between prices, meaning worse execution in many cases. To solve that, you need to read across markets, see the full liquidity picture, even if it's fragmented, and route across it," Saxe said.

For institutional participants, this complexity directly constrains the volume of capital that can flow onchain. As Saxe articulated, stablecoin transaction flows must achieve significantly greater predictability before institutions possess the risk management capabilities and confidence necessary to transfer or maintain substantial amounts onchain.