Asset Tokenization Isn't a 'Magic Solution' for Liquidity Problems: Paris Blockchain Week 2026

Experts at Paris Blockchain Week emphasized that while tokenization enhances accessibility and issuance capabilities, it doesn't automatically generate vibrant secondary trading markets for traditionally illiquid assets.

The process of tokenization does not inherently transform difficult-to-trade assets into liquid ones, according to industry leaders speaking at Paris Blockchain Week, who challenged the notion that deploying private credit, real estate or similar illiquid instruments onto blockchain networks will independently generate thriving secondary trading markets.

During a discussion panel led by Cointelegraph CEO Yana Prikhodchenko, Oya Celiktemur, who serves as Ondo Finance's sales director for Europe, the Middle East and Africa (EMEA), noted that a persistent misunderstanding exists regarding tokenization's ability to enhance the tradability of illiquid assets.

"I think there's still this idea that tokenizing something illiquid will somehow magically make it a liquid asset, which is just not true," said Celiktemur. She added that assets like real estate and private credit "were never that liquid" to begin with.

Francesco Ranieri Fabracci, who leads tokenization expansion efforts at Tether, echoed a comparable perspective. "It's not that if you put an asset onchain, it will be liquid," he said, arguing that only a narrower set of instruments, including bonds, money market funds and stablecoins, are likely to achieve consistent liquidity in tokenized markets.

These remarks emerge as the real-world asset (RWA) tokenization industry continues its expansion phase, with market attention gradually pivoting from simply measuring issuance volume toward evaluating whether these tokenized financial products can generate substantial trading activity and extend beyond restricted distribution networks.

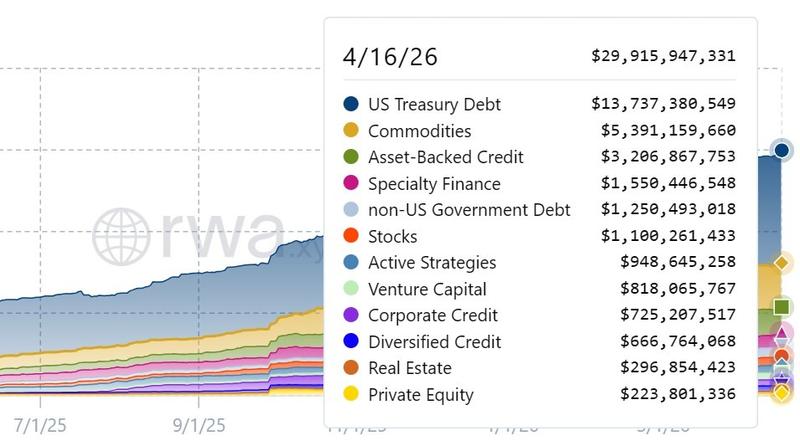

Growth in tokenized RWA market shows concentration patterns

According to data compiled by RWA analytics platform RWA.xyz, the tokenized RWA marketplace grew from $8.8 billion on April 16, 2025, to roughly $29.9 billion on April 16, 2026, representing more than a threefold increase over the course of one year.

This expansion was primarily driven by comparatively standardized and broadly traded asset classes. Tokenized US Treasury Debt and commodities represented a substantial portion of the overall market throughout the entire year.

In stark contrast, asset categories traditionally characterized by lower liquidity levels remained proportionally smaller despite experiencing robust percentage-based growth. Tokenized real estate climbed from about $35 million to $296 million, while private equity advanced from nearly $60 million to $223 million.

Additional market segments, including asset-backed credit and corporate credit, similarly experienced dramatic expansion in absolute dollar terms, signaling increasing issuance activity spanning a wider spectrum of financial instruments.

However, market capitalization figures alone do not serve as proof of genuine liquidity. Total outstanding value can experience growth simply because additional assets are being issued, even when secondary market trading activity continues to be sparse.