Cryptocurrency Industry Pushes for Unmodified Passage of Mining and Staking Tax Legislation

Three leading cryptocurrency advocacy organizations are calling for the approval of legislation that would permit taxation of mining and staking rewards at the point of sale, requesting no additional modifications to the bill.

Three major cryptocurrency advocacy organizations have called on Congressional lawmakers to approve legislation addressing crypto mining and staking taxation without any modifications, asserting that the measure would bring much-needed clarity to the taxation of crypto rewards and guarantee that blockchains "can be secured by Americans in America."

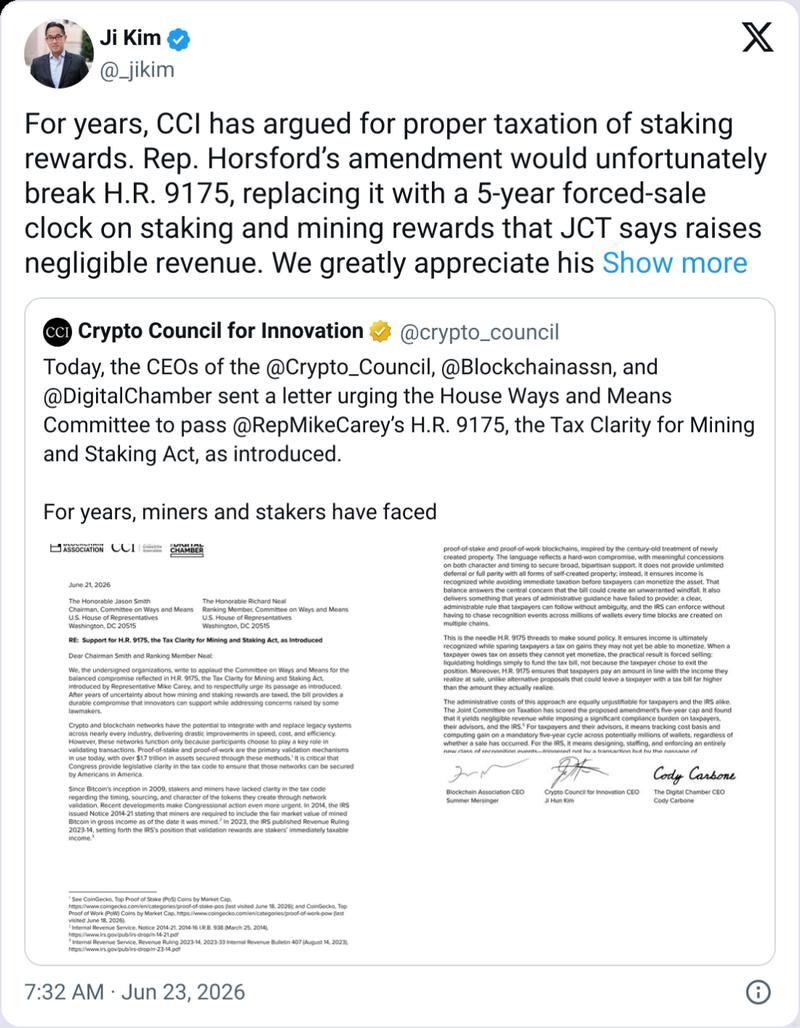

In a letter sent on Sunday to House Ways and Means Committee Chair Jason Smith and the committee's ranking Democrat, Richard Neal, the Blockchain Association, the Crypto Council for Innovation and The Digital Chamber expressed their position that the Tax Clarity for Mining and Staking Act should be approved "as introduced."

"After years of uncertainty about how mining and staking rewards are taxed, the bill provides a durable compromise that innovators can support while addressing concerns raised by some lawmakers," the group wrote.

The proposed legislation aims to resolve what the cryptocurrency sector has consistently characterized as an inequitable tax framework that treats mining and staking rewards as taxable income at the moment of receipt, which according to the letter represents a "taxation of phantom income" that has the potential to create liquidity challenges.

Under the provisions of the bill, individuals engaged in mining and staking activities would have the option to pay taxes on cryptocurrency rewards either at the time they are received or at the point when they liquidate the assets, which the advocacy groups noted "ensures income is recognized while avoiding immediate taxation before taxpayers can monetize the asset."

The legislation was put forward earlier this month in advance of a legislative hearing, though it has yet to move beyond the Ways and Means Committee. Democratic Representative Steven Horsford has submitted an amendment that would impose a five-year limitation on the deferral of crypto reward taxation.

In a post published on X on Monday, Crypto Council for Innovation CEO Ji Hun Kim stated that Horsford's amendment would "break" the bill and generate "negligible revenue."

"We greatly appreciate his engagement, but there have already been significant concessions made in framing this as an election," he added.

The proposed legislation has encountered opposition from traditional banking advocates, with the American Bankers Association stating earlier this month that it would provide "a significant advantage over nearly every other way Americans save, invest and earn returns today."

"When a company pays a dividend, shareholders receive the value of the dividend and pay tax that year," the ABA said. "The Tax Clarity for Mining and Staking Act, would work very differently — and show clear favoritism for cryptocurrencies over other asset classes."

The cryptocurrency advocacy groups contended that attempting to renegotiate any mutually accepted compromise contained within the bill "would risk reviving the very problems the bill resolves and stalling a bipartisan result that is finally within reach."

This piece of legislation comes in addition to another cryptocurrency tax-related bill currently before Congress, known as the PARITY Act, which was put forward in May and instructs the Internal Revenue Service to conduct a study examining what exemptions could be provided for minor cryptocurrency transactions.

The digital asset industry has been advocating for Congress to create exemptions for small-scale crypto transactions from taxation. In April, Kraken revealed that it transmitted 56 million tax forms to the Internal Revenue Service, with nearly one-third pertaining to transactions valued at less than $1, while more than 75% related to transactions under $50.