Why tokenization succeeds with liquid assets, not experimental ones

Assets with substantial market demand facilitate real-time settlement, robust collateral frameworks, and powerful network effects. Adding smart contract functionality to currencies and government debt eliminates inefficiencies in markets where trillions are already transacted.

Opinion by: Sebastián Serrano, founder and CEO of Ripio.

Throughout the majority of the last ten years, blockchain enthusiasts have attempted to tokenize obscure and niche asset classes, hoping to revolutionize the financial system. Although this strategy showed imagination, it fundamentally overlooked the essential economic principle regarding where tokenization genuinely delivers value.

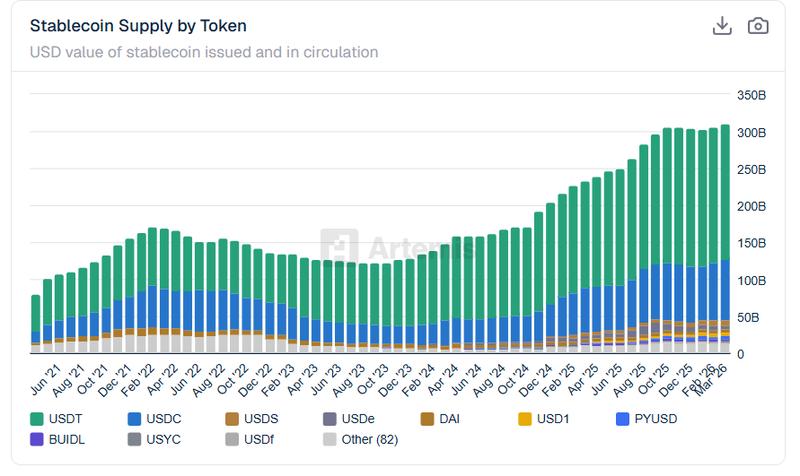

During these initial phases of distributed ledger technology implementation, tokenization demonstrates its greatest effectiveness not at the periphery of economic activity, but rather at its very foundation. The sector's initial impulse — directing efforts toward tokenizing assets with limited liquidity — represented a strategic error. The most triumphant tokenization initiative centered on the world's most liquid asset (the US dollar) through USD-backed stablecoins.

At present, enterprises are testing tokenized iterations of additional highly liquid instruments such as Treasury bills, secondary currencies and, with increasing frequency, equity securities. This pattern is far from coincidental. Tokenization delivers maximum impact when deployed for assets that possess enormous existing demand alongside well-established legal and financial infrastructure. Liquidity represents the fundamental requirement that enables tokenization to evolve from experimental concept to critical infrastructure.

Tokenize what people want

The tokenization process should begin with assets that command substantial existing demand. Currency, government-issued debt, and primary financial instruments constitute the foundational layer of worldwide economic activity. These assets see daily utilization by governmental bodies, business enterprises, and retail participants. When tokenizing these instruments, the objective is not generating demand where none exists. Instead, it involves modernizing the infrastructure through which trillions of dollars currently circulate.

Examining our recent past reveals that electricity was clearly not initially deployed to energize elaborate artistic displays, but rather industrial facilities. Distributed ledgers follow an identical pattern. They achieve maximum utility when applied to tokenizing currency and fundamental financial building blocks, rather than uncommon niche assets.

Stablecoins achieved success precisely because they aligned directly with an established, enormous application. Stablecoins facilitate dollar transfers internationally, with speed and minimal cost. Tokenized government securities are building momentum for identical reasons. They embody genuine, high-demand instruments that financial institutions already maintain in substantial quantities.

Tokenization delivers maximum benefit in areas where inefficiencies are both significant and costly. Bond markets facilitate trillions in transactions, yet they operate with considerable inefficiency. Tokenization reduces settlement timeframes from multiple days to mere minutes. Tokenization enables simultaneous movement of assets and currency, instantaneously, without dependence on third-party intermediaries. This transformation fundamentally alters both the expense structure and risk characteristics of financial transactions.

NFTs and extremely specialized RWAs represent the polar opposite. Their fragmentation is inherent to their design. Every individual asset possesses uniqueness, legal uncertainty, and resists standardization. These characteristics prevent them from functioning as a universal economic foundation. While they may possess cultural significance or speculative appeal, they cannot support extensive financial network effects.

Market effects of tokenizing liquid assets

When adding smart contract capabilities to assets lacking liquidity, fractional ownership becomes possible and certain operational processes can be automated. This does not, nevertheless, create novel forms of economic cooperation. The underlying asset continues to experience infrequent trading activity. Deep, robust markets remain absent.

When dealing with liquid assets, conversely, tokenization enables completely new financial mechanisms. Perpetual settlement processes, payment streaming, and automated management of collateral represent merely some of the innovations that tokenization facilitates.

Additional factors warrant consideration. Is it possible to utilize a specific tokenized asset for collateral purposes? This represents a crucial question, with the response being that liquidity primarily determines the answer. Liquid assets, after all, integrate securely as collateral within automated frameworks. Their market valuations remain transparent with real-time updates.

Assets lacking liquidity, in contrast, experience irregular trading activity, subjective pricing assessments, and substantial spreads between bid and ask prices. These inherent characteristics render them exceptionally problematic for collateral applications. Tokenization fails to resolve this fundamental challenge. Consequently, this diminishes overall demand for such assets.

Capital utilization efficiency also experiences dramatic improvement when applied to liquid instruments. Tokenized liquid securities can theoretically undergo rehypothecation, fractional deployment, and algorithmic allocation instantaneously. Capital flows more rapidly throughout the entire system. Tokenization cannot, however, generate continuous trading markets for assets that inherently lack liquidity.

Reducing risk through clarity

US dollars, sovereign bonds, and major corporate obligations possess clearly defined legal standing, issuer responsibility, and comprehensive regulatory structures. Tokenization integrates within current financial legislation, which makes institutional implementation considerably more direct and feasible.

The situation proves more challenging for NFTs. Uncertainties surrounding ownership rights, custody arrangements, legal enforceability, and investor safeguards can overshadow any technical advantages. In real-world application, these ambiguities amplify risk instead of diminishing it. It stands to reason that substantial, institution-focused tokenization initiatives prioritize liquid assets initially.

The trajectory of tokenization will ultimately be shaped by assets occupying central economic positions. Naturally, the blockchain industry's initial experimentation with NFTs served a necessary and comprehensible purpose. Long-term success for NFTs proved difficult to achieve. Their focus targeted an inappropriate asset category.

Stablecoins demonstrated this principle by enhancing the world's most liquid asset. Tokenized sovereign bonds and stock securities represent the natural progression forward. This approach enables blockchains to transition from experimental innovation to essential financial infrastructure.

Opinion by: Sebastián Serrano, founder and CEO of Ripio.