The Collapse of Tokenized SpaceX Stock: What Prevented Retail Access

Despite attracting over $1 billion in investor interest, tokenized SpaceX shares never reached most buyers who received refunds. Here's what happened.

The $1B SpaceX tokenization revealed cryptocurrency's critical vulnerability

Retail participants excluded from private equity markets found tokenized SpaceX shares to be an exceptional pathway into one of the planet's most sought-after private corporations. These blockchain-powered tokens enabled participants to pursue exposure outside traditional brokerage systems and ahead of any future public market debut.

Reality intervened with logistical challenges.

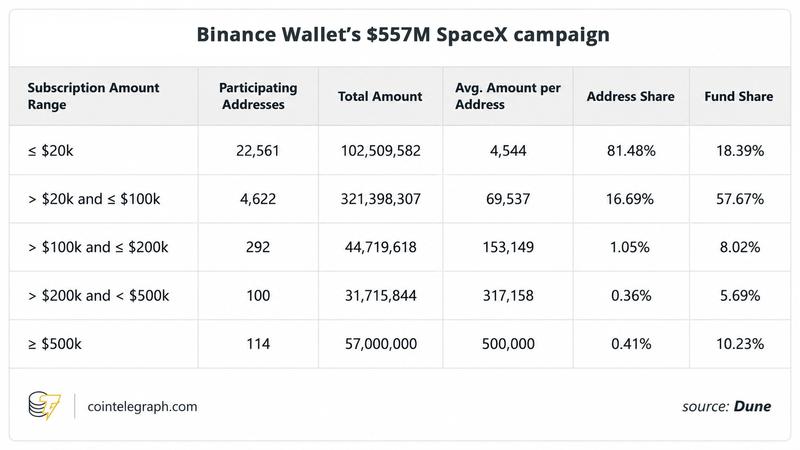

During June 2026, xStocks reported that client interest exceeded $1 billion for its tokenized SpaceX share product. Cryptocurrency exchanges including Bybit, Binance Wallet and Bitget Wallet promoted participation in the program, generating substantial enthusiasm among community members eager to gain access to Elon Musk's space exploration enterprise.

Many participants ended up receiving zero shares.

Multiple distribution platforms canceled their programs and processed refunds when they proved unable to source sufficient underlying SpaceX equity to back the tokens. This situation rapidly evolved into an important real-world examination of tokenized securities. It underscored a fundamental truth about blockchain-based investing: While tokenization can transform ownership into digital formats, it cannot manufacture assets that do not exist.

What transpired with the SpaceX tokenized share initiative

Anticipation for a SpaceX Initial Public Offering (IPO) had historically been expected to capture widespread market attention. The aerospace corporation stands at the intersection of multiple major sectors: private space exploration, Starlink satellite internet services, military technology and Elon Musk's worldwide influence. Countless participants had pursued direct ownership stakes for an extended period.

Responding to this demand, xStocks launched SPCXx, a blockchain-based representation of SpaceX equity. This instrument was designed to provide digital exposure to the enterprise, enabling transactions through cryptocurrency exchanges rather than traditional stock brokers.

Interest levels skyrocketed immediately.

Industry reports suggested that subscription requests exceeded $1 billion ahead of final distribution determinations. Binance Wallet independently reportedly attracted over half a billion dollars in participant commitments. Buyers perceived the program as an uncommon method to access one of the globe's most valuable privately-held enterprises.

Subsequently, distribution announcements arrived.

Various participating exchanges reported failure to secure adequate underlying equity positions necessary for token creation. Lacking actual share ownership to support the instruments, the tokenized program could not proceed.

Mass cancellations and refund processing followed.

The mechanics behind tokenized stock products

Tokenized equities represent blockchain-powered alternatives to conventional share ownership. Instead of purchasing stock through traditional brokerages, participants acquire digital instruments that signify ownership rights or economic participation connected to genuine shares maintained off-blockchain.

The typical workflow operates this way:

- A licensed custodian acquires the physical shares.

- A tokenization service generates blockchain instruments backed by those holdings.

- Participants purchase and exchange the tokens.

- The instrument's value is structured to mirror the underlying equity's performance.

The theoretical benefits are substantial, though they involve significant considerations.

Tokenized securities enable continuous trading cycles, worldwide accessibility, partial ownership capability and simplified integration with cryptocurrency wallets and decentralized financial platforms.

For participants in territories with restricted access to American capital markets, tokenization presents a viable channel to instruments that were historically challenging or unattainable.

Did you know? The concept of tokenized securities existed before blockchain technology. Banking institutions tested digital representations of equities and debt instruments for many years, but distributed ledger technology enabled worldwide, direct ownership transfers with improved ease and visibility.

xStocks' strategy for delivering SpaceX investment access

The SPCXx program was constructed around a simple concept. For every token issued, xStocks planned to secure matching SpaceX equity to function as backing for the digital instruments traded by buyers.

From the participant's perspective, the mechanism appeared uncomplicated. Community members deposited capital, entered the subscription queue and anticipated receiving tokenized SpaceX participation following distribution choices.

The framework held particular attraction because numerous retail buyers assumed tokenization might democratize access to premium IPOs traditionally limited to institutional capital and wealthy individuals.

What numerous participants underestimated was that the tokenization workflow still demanded authentic equity acquisition before token generation could occur.

This requirement proved to be the critical constraint.

The reason demand exceeded accessible inventory

The core issue was not the tokenization mechanism. It was the scarcity of genuine SpaceX equity required to support the tokens. When participant enthusiasm for a corporation reaches extraordinary levels, only a limited quantity of equity can be allocated. Not all participants can obtain their desired amount.

Conventional IPOs routinely encounter this restriction. Brokerage firms frequently receive fewer shares than customer requests. Institutional capital sources compete intensely for distributions. Retail buyers often obtain reduced positions or nothing whatsoever.

The SpaceX situation amplified this dynamic.

Via blockchain infrastructure, xStocks dramatically broadened the pool of potential buyers. Tokenization extended involvement beyond a narrow cohort of brokerage customers to a worldwide cryptocurrency community.

Interest grew exponentially, while inventory remained constrained. The physical shares continued to be controlled by conventional equity market limitations. This discrepancy ultimately proved insurmountable.

The reason tokenization cannot manufacture unavailable shares

A widespread misunderstanding regarding tokenized equities is that distributed ledger technology somehow eliminates scarcity. This is inaccurate.

Blockchain technology can enhance settlement processes, expand accessibility and increase trading efficiency. It can digitize ownership documentation and enable fractional positions. It cannot, however, generate additional legal ownership stakes in a corporation.

Every legitimately supported tokenized share demands a corresponding underlying instrument. When a tokenization service cannot purchase the shares, it cannot create authentic tokens.

This distinction matters because tokenization is frequently marketed as a transformative answer to financial market limitations.

The SpaceX situation demonstrated that certain restrictions persist in physical reality. No quantity of blockchain infrastructure can produce additional SpaceX equity when inventory is depleted.

Did you know? SpaceX continues to be among the most frequently traded private corporations in secondary exchanges. Company employees, initial backers and venture capital firms regularly exchange shares through private transactions, establishing a robust private secondary marketplace ahead of the firm's potential public debut.

The challenges encountered by Bybit, Bitget Wallet and distribution collaborators

The difficulties experienced by distribution platforms also illuminate another critical concern in tokenized finance: dependence on extended operational sequences.

Bybit, Bitget Wallet, Binance Wallet and additional distribution collaborators lacked direct authority over the distribution workflow. Rather, they depended on xStocks and other infrastructure services to source the underlying equity.

When those shares proved unavailable, the entire distribution infrastructure collapsed. Community members frequently assumed they were transacting directly with the instrument itself.

Multiple intermediaries functioned within the arrangement:

- The tokenization service provider

- The custodian maintaining the shares

- The distribution source

- The exchange or wallet facilitating access

When any component of that chain malfunctions, the complete participant experience can deteriorate accordingly. In this instance, the breakdown occurred before token creation began.

The way refunds safeguarded users yet revealed platform vulnerabilities

To their advantage, involved platforms typically executed refunds promptly. Some proceeded further by providing supplementary compensation, incentives or fee reversals to mitigate the disappointment.

From a financial perspective, most customers escaped direct monetary losses. From a credibility standpoint, nevertheless, the circumstances were more complex. Participants learned that marketed "access" did not guarantee actual involvement.

Numerous individuals had interpreted promotional campaigns as verification that shares would materialize. The cancellations clarified that securing inventory remained uncertain until final distributions were finalized.

This experience could influence how participants evaluate upcoming tokenized programs. Confidence represents one of the most critical components in capital markets, and incidents like this can undermine it even when refunds are processed.

Did you know? Fractional ownership is not exclusive to cryptocurrency. Conventional brokers have provided fractional shares of high-priced equities such as Amazon and Berkshire Hathaway for extended periods, enabling participants to purchase portions of a share instead of complete units.

Comparing tokenized shares with traditional shares

An additional insight from the SpaceX situation involves understanding what tokenized shares genuinely represent. Numerous participants presume that acquiring a tokenized stock equals possessing a conventional share.

This is not invariably accurate.

Based on the framework, token owners may not obtain:

- Voting privileges

- Direct corporate communications

- Corporate governance participation

- Specific shareholder benefits

Alternatively, tokenized instruments may deliver economic exposure to valuation fluctuations instead of complete legal shareholder standing. This distinction becomes particularly significant during corporate actions, acquisitions, dividend distributions or regulatory matters.

Participants should examine the legal structure underlying any tokenized equity program before allocating capital.

Essential risks retail participants must recognize

The SpaceX incident highlighted several risks with greater clarity. These risks extend beyond this specific program:

- Allocation risk: High-demand instruments frequently attract more interest than existing inventory.

- Counterparty risk: Participants depend on creators, custodians, exchanges and tokenization services.

- Regulatory risk: Frameworks for tokenized securities remain under development across numerous territories.

- Liquidity risk: Transaction volume can fluctuate dramatically between different instruments.

- Redemption risk: Participants require transparency regarding how tokens can be converted and what entitlements accompany ownership.

None of these concerns are exclusive to tokenized finance. Nevertheless, the blockchain presentation can occasionally make them less apparent to participants with minimal expertise.

Insights the SpaceX situation provides about tokenized securities

Despite the program's failure, the broader implication may actually prove positive for the tokenization industry. Interest exceeding $1 billion demonstrated powerful participant appetite for blockchain-enabled access to conventional instruments.

The marketplace clearly desires tokenized securities.

Community members appreciate the concept of managing equities through cryptocurrency wallets. They value continuous trading availability, global accessibility and reduced participation barriers.

The challenge resides in consistently connecting that enthusiasm to genuine instruments in the physical economy.

Subsequent tokenized programs could improve through:

- More robust sourcing arrangements

- Increased transparency in allocation workflows

- Superior disclosure of inventory constraints

- More comprehensive explanations of participant entitlements

The fundamental technology largely functioned as intended.

What failed was the capacity to procure sufficient quantities of the underlying instrument.