Botanix's Demise: Evidence That Bitcoin Holders Reject DeFi?

Botanix's collapse indicates that Bitcoin holders still gravitate toward Ethereum-based DeFi over Bitcoin layer-2 solutions. What strategies can Bitcoin L2s employ to attract hodlers?

Throughout the previous two market cycles, decentralized finance on Bitcoin has existed primarily as an aspiration rather than an established sector.

The concept of programmable Bitcoin has persisted as an ambition championed by a particular segment of Bitcoin maximalists who maintain that the leading cryptocurrency by market capitalization can achieve utility without compromising its security characteristics or sound money attributes.

However, the recent shutdown of Botanix, a Bitcoin scaling infrastructure, earlier this month has cast doubt on this ambitious vision.

When a well-capitalized, technically sophisticated Bitcoin layer-2 solution with operational applications, established integrations and attractive returns cannot generate sufficient user engagement to remain viable, does this indicate that Bitcoin holders fundamentally lack interest in decentralized finance protocols?

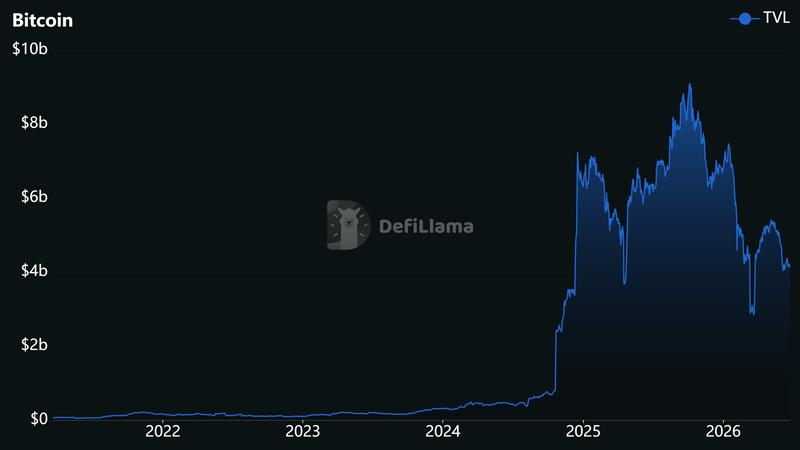

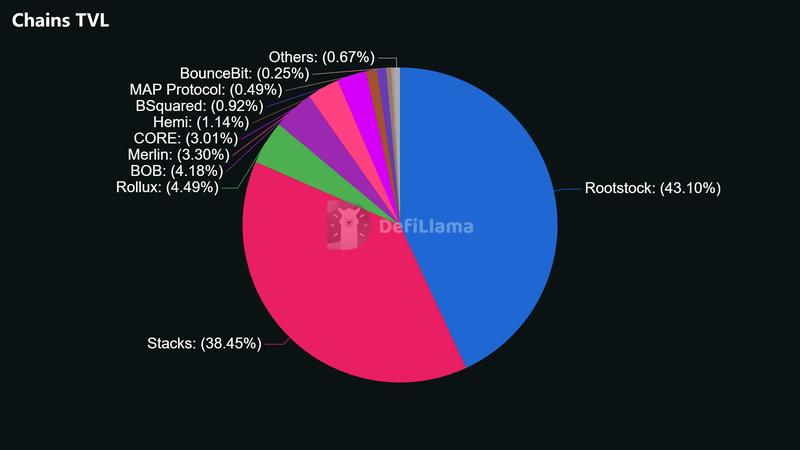

Despite years of promotion as the industry's next major breakthrough, Bitcoin DeFi continues to occupy a marginal position in 2026.

Data from DefiLlama's analytics platform reveals merely $4.12 billion in total value locked (TVL) distributed across Bitcoin DeFi protocols collectively. This figure represents a negligible fraction when compared to Bitcoin's $1.2 trillion market capitalization, and the hundreds of billions of dollars maintained through spot exchange-traded funds, corporate balance sheets and custodial storage solutions.

Andre Dragosch, head of research Europe at Bitwise, told Cointelegraph, "Bitcoin is winning decisively as a monetary asset and as pristine collateral, but the case for Bitcoin as a standalone DeFi execution layer was always structurally weaker than the narrative suggested."

Botanix closes after four years

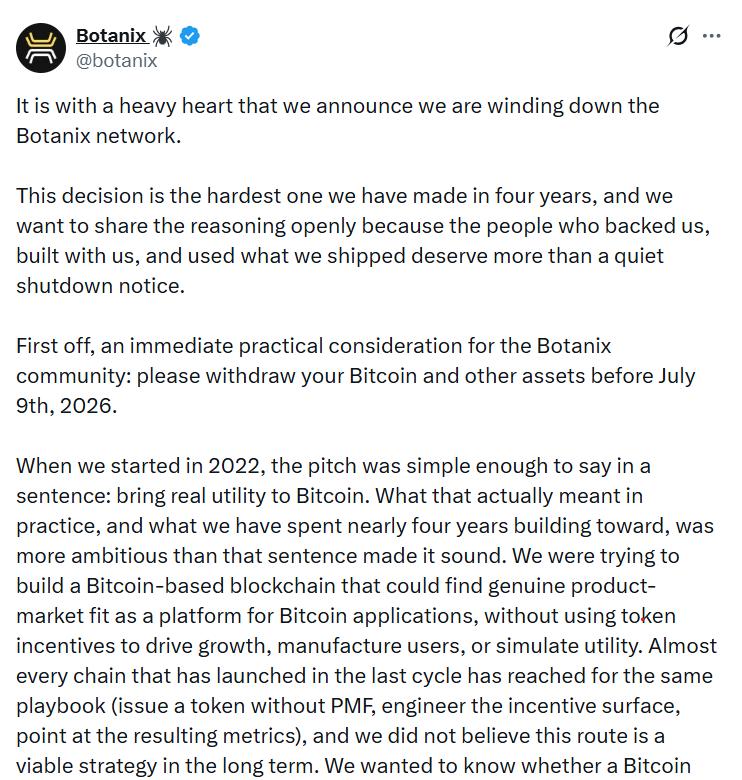

The announcement from Botanix regarding its shutdown came after approximately four years of development work and one year of mainnet operation, with the team citing demand shortfalls rather than security breaches or regulatory pressures as the primary cause.

The platform Botanix described was a network that functioned correctly from every technical perspective: processing 25 million transactions, serving 200,000 distinct wallets, and facilitating the bridging of tens of millions of dollars in assets, yet it consistently failed to produce the transaction fee revenue necessary to sustain its operational infrastructure.

Participants arrived seeking yield opportunities, utilized BTC primarily as store-of-value collateral, and then predominantly maintained passive, holding-oriented approaches, rather than actively engaging in borrowing activities, trading operations, or transferring assets with sufficient frequency to create substantial fee revenue.

Similar to most contemporary BTCFi infrastructure, Botanix required participants to transfer their Bitcoin into a tokenized representation on a distinct Ethereum Virtual Machine (EVM)-compatible blockchain before gaining access to DeFi functionality. This process introduces supplementary bridge-related and smart contract trust assumptions that concern numerous Bitcoin advocates.

Nevertheless, Botanix co-founder Willem Schroé told Cointelegraph that he would not have altered the fundamental architecture. Despite Botanix providing what he characterized as "the best rates in the industry" along with a security model more aligned with Bitcoin principles than conventional wrapped BTC bridges, wrapped BTC operating on Ethereum still maintained competitive superiority over Botanix.

He credited this outcome to Ethereum's "huge infrastructure network and Lindy effect," combined with a blend of liquidity depth, user experience quality and regulatory familiarity.

What Botanix learned about Bitcoin DeFi

The development team reached the conclusion that Bitcoin continues to be perceived as a reserve asset instead of an asset with programmable functionality.

For the majority of current applications including lending protocols, leveraged position creation, or yield generation, a wrapped BTC position within a large, established EVM ecosystem such as Ethereum proves "genuinely sufficient" for most participants. Instead of bridging assets into a Bitcoin-oriented EVM chain like Botanix, users demonstrated a preference for maintaining wBTC positions on platforms where liquidity pools, decentralized applications and ecosystem integrations are already established.

Botanix additionally highlighted the concentration of onchain activity around platforms like Hyperliquid, along with major centralized exchange operators and consumer-oriented fintech platforms that "own the user relationship," resulting in independent infrastructure providers "rowing upstream" against the forces of convenience and brand recognition.

Wilhelm said he hopes Botanix's wind-down "will definitely be looked at by others," and characterized the entire process as a professionally executed experiment whose insights other BTCFi developers should consider carefully.

Bitcoiners, DeFi and wrapped BTC

Though estimates differ, only a minimal percentage of Bitcoin's circulating supply is presently deployed productively in DeFi protocols, and the majority of that capital resides in wrapped BTC instruments on Ethereum and its layer-2 networks like Base and Arbitrum, in addition to Polygon, Solana and BNB Smart Chain. A smaller proportion exists on "Bitcoin L2" networks, with Bitcoin-focused L2s and sidechains representing a modest portion of that activity measured by value.

Tokenized BTC products themselves constitute merely a tiny fraction of the total asset: Analysis conducted in May 2026 calculated that approximately $20 billion worth of BTC — representing less than 2% of Bitcoin's total circulating supply — exists on EVM chains in wrapped formats.

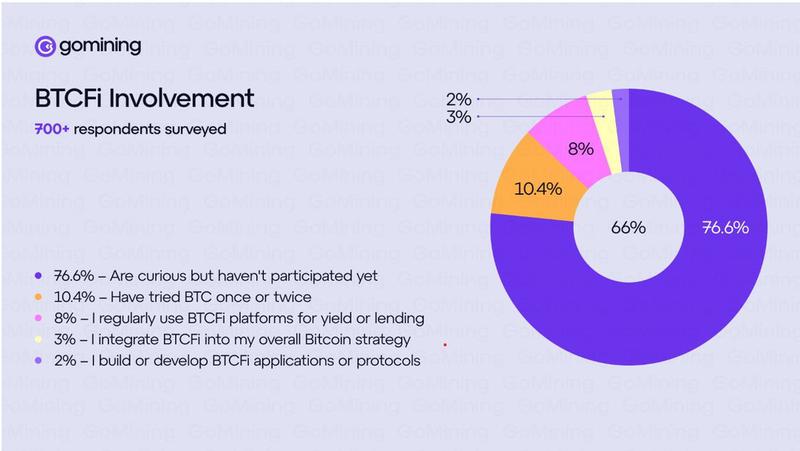

A GoMining survey conducted in October 2025 involving 730 Bitcoin holders revealed that 77% of survey participants had never utilized a BTCFi platform, with only 3% incorporating BTCFi strategies into their comprehensive Bitcoin approach.

Even accounting for potential sample bias (these survey participants were engaged, survey-completing BTC holders), the data demonstrates that BTCFi platforms designed to maintain users within Bitcoin-aligned technology stacks continue to represent a specialized activity instead of widespread adoption.

Justin d'Anethan, head of research at crypto private markets advisory firm Arctic Digital, told Cointelegraph, "There is more liquidity and better yields on EVM or SVM [Solana Virtual Machine] native solutions than on BTC solutions, period."

When institutional clients inquire about "putting their Bitcoin to work," the viable pathways, he explained, continue to be centralized trading desks, exchange platforms offering BTC lending at 2% to 4% rates, basis trade structures "à la Ethena," or institutional credit facilities like Maple.

He identified the primary barrier for most Bitcoin holders as the risk associated with bridging to a less secure Bitcoin L2. For "hardcore BTC maxis," the standard approach remains cold storage solutions, HODLing strategies and relying on price appreciation, instead of attempting to "eke out 2-3% with counterparty risk."

Native BTCFi as a structural mismatch

Dragosch indicated that Botanix's collapse pointed toward demand for independent Bitcoin DeFi execution layers being considerably weaker than proponents had anticipated.

He contended that capital that "genuinely wants yield has migrated to wrapped BTC on mature, liquid venues rather than bridging into bespoke federations."

From this perspective, the challenge isn't simply that Bitcoin holders haven't yet "discovered" native DeFi opportunities; it's that the technological architecture and user community are fundamentally misaligned. Bitcoin's foundational layer operates slowly, conservatively and remains firmly rooted in the store-of-value narrative framework.

"Bitcoin as reserve collateral is the durable trade," Dr. Dragosch said, "the next leg of adoption runs through institutions and balance sheets, not necessarily through onchain execution layers."

Who is still building BTCFi, and for whom?

Diego Gutierrez Zaldivar, chief executive of RootstockLabs, which operates a Bitcoin-secured, EVM-compatible sidechain, rejects the notion that "no demand" exists for Bitcoin-backed lending services, yield generation products or broader BTCFi offerings.

He identified the primary limitation as trust: establishing the operational infrastructure, legal frameworks and risk management systems that institutional participants require.

More than 40% of total Bitcoin DeFi activity currently operates through Rootstock, he noted, encompassing real-world asset settlement transactions and institutional custody vaults. Throughout the past year, he explained, investment funds have begun requesting to deposit hundreds or even thousands of BTC simultaneously into Rootstock-based products; capital flows that were practically nonexistent two or three years previously.

Orkun Mahir Kılıç is co-founder of Chainway Labs, the organization behind Citrea, a Bitcoin-anchored rollup that maintains user assets within Bitcoin's security framework and validates its state using zero-knowledge proof technology. He contended that replicating EVM DeFi primitives onto Bitcoin represents a strategic dead end, and characterized Botanix's outcome as a judgment on that particular model, rather than BTCFi as a concept.

He told Cointelegraph that "more secure" doesn't alter most participants' behavior patterns.

"People don't price counterparty risk until something breaks," he said. "Where it matters" is for institutional entities and large-scale holders that require trust-minimized transaction execution with no custodial intermediary that can fail.

"For everyone else, the reason to be here isn't the security guarantee in the abstract; it's the applications that don't exist elsewhere."