Beyond US-Mexico: Bybit Identifies $112B Stablecoin Remittance Opportunity Across Latin America

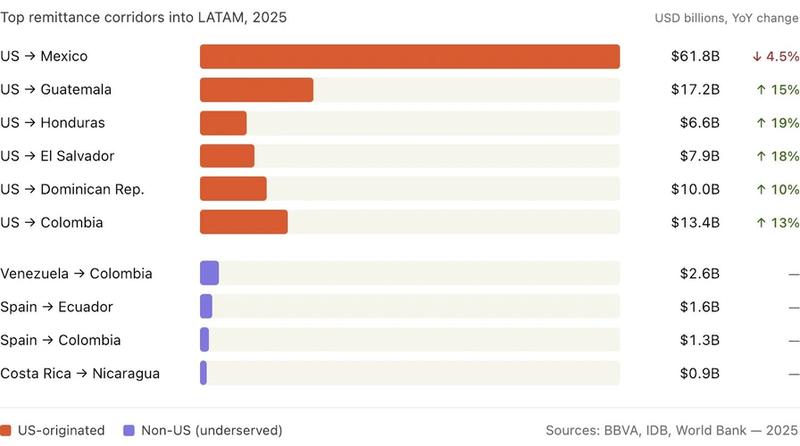

While remaining the dominant route, the US-Mexico remittance channel experienced a 4.5% contraction in 2025 as alternative Latin American pathways expanded.

A top executive at Bybit suggests that financial technology and stablecoin companies ought to expand their focus beyond the traditional US-Mexico remittance route to capture a larger share of Latin America's $174 billion money transfer industry.

According to Bybit's Chief Marketing Officer Claudia Wang, who shared insights via an X platform post on Sunday, the majority of companies have concentrated their efforts too heavily on the $61.8 billion US-Mexico money transfer sector. In doing so, these firms are overlooking rapidly expanding pathways connecting the United States with Central American nations, along with intra-regional Latin American remittance flows.

"The corridors that look 'hot' right now are not the corridors most fintechs are optimized for," she said, citing Venezuela-to-Colombia, Argentina-to-Bolivia and Spain-to-Ecuador as examples. The non-US-to-Mexico remittance market stands at about $112 billion.

"Stop treating LATAM as one market," Wang said, adding that she spent six months studying the region:

"Brazil, Mexico, Argentina, Colombia — each needs different licenses, different rails, different stablecoins, different marketing. The companies winning here run country-specific stacks, not regional ones."

Money transfer services across the Americas have historically been dominated by traditional banking infrastructure operated by established players like Western Union and MoneyGram. That said, both organizations announced initiatives to implement stablecoin-based technology infrastructure after the GENIUS Act became law in July.

Western Union is building its own US dollar-backed stablecoin, USDPT, which is in the final stages of readiness and expected to launch this month.

Wang pointed out that cryptocurrency-focused enterprises including Binance, Bitso, Strike and Felix Pago are actively participating in the Latin American remittance space, alongside traditional financial institutions and major retail and telecommunications corporations like Walmart and Tigo.

US immigration policy is influencing LATAM remittance market

According to Wang's analysis, the remittance corridor connecting the United States with Central America "is exploding," evidenced by transfer volume increases in Honduras, El Salvador and Guatemala of 19%, 18% and 15%, respectively, in 2025.

In stark contrast, money transfers flowing through the heavily saturated US-Mexico pathway declined 4.5% to $61.8 billion.

Wang said the divergence between rising Central American flows and Mexico's decline is the result of US immigration policy: "Migrants from Central America are sending more home — faster, larger amounts — to hedge against deportation risk."

Conversely, according to Wang, Mexico benefits from a "more established and documented diaspora" and therefore "doesn't show the same panic-send behavior."

Regarding the remittance corridors that don't involve the United States, Wang observed that although certain transfer markets appear modest when measured in total dollar volume, they remain "barely served" by American money transmission businesses and are "almost untouched by crypto rails."

Latin Americans want to hold stablecoins, not just move them

Wang also emphasized that numerous Western financial technology firms have failed to recognize that throughout Latin America, the true "killer app" involves maintaining stablecoin holdings rather than simply facilitating their transfer.

"Users don't want to 'use' stablecoins for a transaction and convert back to local currency. They want to hold dollars. The transaction is the side effect."

Wang said there is no clear winner in the LATAM remittance market, adding that "the fintechs that win the next decade in this region will combine local rails, stablecoin liquidity, trust and closed-loop economics — remit → hold → spend → earn."

She further noted that a significant number of fintech businesses operating in this sector have developed their platforms with the stereotypical 25-year-old cryptocurrency enthusiast in mind, rather than designing for the actual remittance customer, who typically falls between 40 to 60 years of age and presumably lacks advanced technical proficiency.

"If your product makes a 50-year-old factory worker in New Jersey think for more than 30 seconds before sending $300 to his mom in Honduras, you've already lost," Wang said:

"The crypto industry has spent five years optimizing for the wrong user. The retail remittance customer in LATAM doesn't want to 'self-custody.' They want to know the money landed."