Bridging Europe's SME Financing Deficit Through Blockchain-Based Capital Solutions

A €39 billion yearly financing shortfall affects small and medium enterprises across Europe, beyond traditional banking institutions' capacity. Cointelegraph Research's latest analysis examines how RWA credit frameworks might address this critical gap.

Following the Great Financial Crisis of 2008, European banking institutions faced regulatory requirements to maintain increased capital reserves against higher-risk lending activities. This regulatory shift made small and medium enterprise financing less economically viable, as these loans demanded comparable underwriting and oversight expenses to larger corporate loans while delivering lower total returns. While private credit organizations stepped in to partially address this void, they subjected borrowers to variable interest rates that became unsustainable during periods of rate increases. Today, small and medium enterprises throughout Europe confront a €39 billion yearly financing deficit.

The latest analysis from Cointelegraph Research highlights a structured-access hybrid framework within the RWA private credit sector that holds promise for addressing the funding shortfall through blockchain-based capital deployment. A single platform utilizing this methodology has successfully facilitated 15.4 million USDC in loan originations distributed among 2,143 participating investors.

Read the full Cointelegraph Research report here

RWA Private credit

One of the principal benefits of RWA private credit lies in its fractionalization capability. Within conventional private credit markets, an individual loan exposure remains entirely with a single lending institution or gets allocated among a limited consortium of institutional participants via a fund framework. Fractionalization divides the exposure into smaller increments, with each increment representing a proportional stake in the identical underlying loan instrument, thereby enhancing transferability and expanding the investor pool beyond domestic institutional funding sources. An individual retail participant located in Indonesia can acquire $500 in exposure to a Czech small business loan without engaging a local brokerage, custody provider, or fund administration service, with transaction settlement executing instantaneously through cross-border stablecoin transfers.

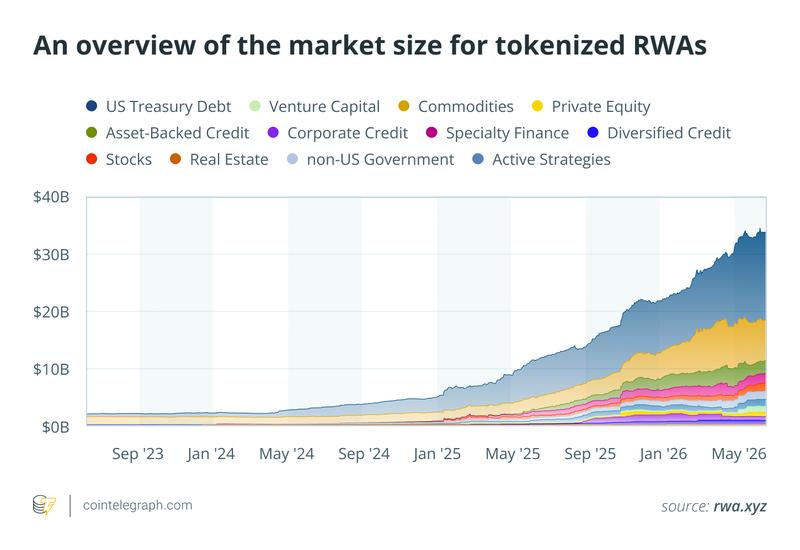

When stablecoins are excluded from calculations, blockchain-based RWA value has expanded from approximately $2.7 billion in January 2024 to roughly $30 billion by April 2026. Government debt instruments constitute the dominant RWA category at $14.8 billion, followed by private credit at $6.1 billion, commodity-backed assets at $5.4 billion, and equity securities at $2.1 billion.

Nevertheless, while RWA expansion demonstrates appetite for yield-generating instruments capable of integrating with cryptocurrency-native capital pools, this growth does not validate that retail accessibility for small and medium enterprises has been adequately addressed. Small and medium enterprises generally secure financing with physical assets including machinery, equipment, vehicles, inventory, or real estate holdings. Yet the majority of current RWA offerings accept financial collateral such as receivables, treasury instruments, or cryptocurrency-native assets. These products also maintain restrictions via accredited investor qualifications, minimum capital requirements, or mandatory KYC verification procedures. For instance, Centrifuge's ACRDX restricts participation to accredited investors outside the United States and imposes a $500,000 minimum investment threshold. Ondo Finance's tokenized treasury offerings mandate KYC verification and prohibit access from multiple jurisdictions. Canton Network focuses on regulated financial counterparties instead of unrestricted retail participation.

Structured-access hybrid model

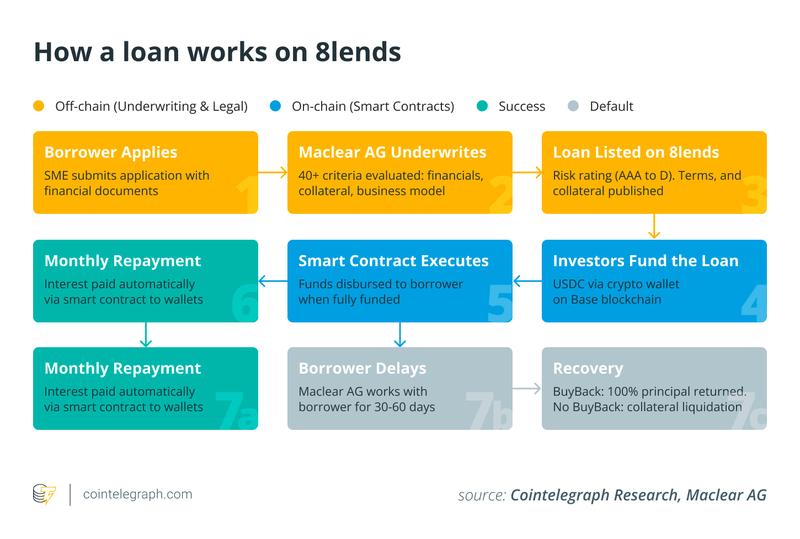

A developing framework within RWA private credit that resolves this discrepancy is termed the structured-access hybrid model. Within this framework, investors allocate stablecoins into smart contract protocols, which subsequently channel capital to regulated lending entities that authenticate borrowers, examine physical assets, and establish legal security interests.

One representative example of a project constructing within the structured-access hybrid model framework is 8lends. It serves as the retail-oriented Web3 interface for Maclear AG, a Swiss-registered financial intermediary established in 2020 and functioning as a financial intermediary under PolyReg SRO regulatory oversight. Within this organizational structure, 8lends operates as the distribution and settlement infrastructure for loans that Maclear underwrites and originates. Investors contribute a minimum of 100 USDC to obtain exposure to these small and medium enterprise loans.

Through Q2 2026, 8lends has facilitated approximately 15.4 million USDC in loan originations. From this total, 5.79 million USDC has been successfully repaid (representing roughly 38%) and 9.61 million USDC continues as active credit exposure (representing roughly 62%), distributed across 2,143 investors.

Read the full report to see how the structured-access hybrid model compares to other RWA architectures, what risks remain as these platforms scale, and whether this approach can fully close the €39 billion SME funding gap.