South Korean regulators crack down on crypto exemption loopholes following fraud epidemic

According to the Financial Services Commission, disparate exemption policies across platforms enabled vulnerabilities that permitted rapid fund transfers from accounts with limited activity records.

Financial authorities in South Korea have announced plans to strengthen exemption policies within the cryptocurrency withdrawal-delay framework following research revealing that accounts receiving special exemptions were responsible for the bulk of losses tied to voice-phishing schemes.

In a statement released Wednesday, the Financial Services Commission (FSC) outlined that the enhanced regulatory approach, created in collaboration with the Financial Supervisory Service (FSS) and the Digital Asset eXchange Alliance (DAXA), will establish standardized criteria determining which users may circumvent withdrawal delay requirements.

According to the regulator, cryptocurrency exchanges had been operating under their own individual exemption policies without established minimum benchmarks, generating security gaps that enabled fraudulent actors to rapidly transfer funds by satisfying lenient conditions such as minimum account longevity or basic trading activity.

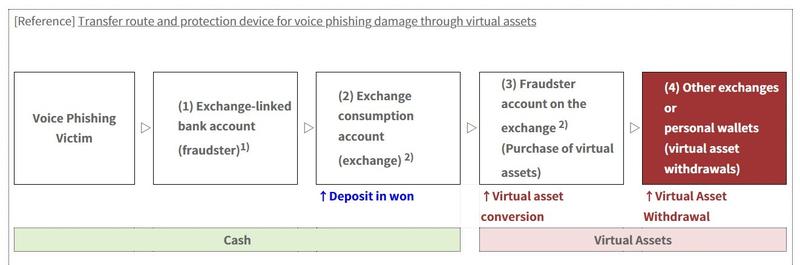

Between June and September 2025, user accounts that received withdrawal-delay exemptions represented 59% of all fraudulent accounts and accounted for 75.5% of fraud-related financial losses across cryptocurrency platforms, according to FSC data.

This regulatory action is part of a broader initiative by South Korean authorities to enhance cryptocurrency exchange oversight following widespread voice-phishing exploitation and failures in operational governance, including new regulatory measures announced this week in response to Bithumb's Bitcoin (BTC) distribution mistake.

Standardized criteria designed to prevent abuse of exemption privileges

According to the FSC's announcement, the updated regulatory framework will require exchanges to evaluate multiple variables including transaction frequency, user account age, and the volume of both deposits and withdrawals when deciding whether an individual qualifies for withdrawal-delay exemption status.

The financial watchdog indicated that implementing these changes is anticipated to dramatically decrease the total number of users who meet exemption eligibility requirements. According to the FSC, modeling analysis demonstrated that user exemption eligibility would decline to approximately 1% following implementation of the new standards, though no comparative baseline figure was disclosed.

The FSC further stated it plans to enhance monitoring protocols for users who receive exemptions by conducting regular audits, including verification procedures to confirm the legitimate origin of deposited funds, and by implementing technological systems designed to identify suspicious withdrawal patterns.

The regulatory body emphasized its commitment to ongoing evaluation of the exemption framework to identify and prevent emerging circumvention tactics and to make modifications as circumstances require.

This initiative represents another component of the comprehensive effort by South Korean financial regulators to strengthen supervision of cryptocurrency trading platforms in the wake of several recent operational failures.

Earlier this week on Tuesday, the FSC mandated that exchanges must perform reconciliation between their internal accounting records and actual cryptocurrency asset holdings at five-minute intervals following an investigation connected to the Bithumb distribution error that revealed deficiencies in internal oversight and risk management protocols.

On Jan. 29, South Korea broadened cryptocurrency licensing oversight requirements to encompass both trading platforms and their primary stakeholders.