How Regulatory Framework Will Unlock Australia's $17B Digital Asset Potential

Clear regulatory frameworks, licensing standards and digital finance infrastructure are essential prerequisites for Australia to realize a A$24B opportunity in cryptocurrency and tokenization.

Key takeaways

- The potential for Australia to generate A$24 billion, equivalent to roughly $17 billion, each year from tokenized finance and digital assets exists, but realization hinges on policymakers creating clear and favorable regulatory structures.

- Financial markets stand to be revolutionized through tokenization by enhancing liquidity, streamlining settlement automation and broadening investor participation in assets including foreign exchange, equities, government bonds and investment vehicles.

- Various forms of tokenized currency, encompassing CBDCs and stablecoins, have the potential to dramatically decrease both the expense and duration of international payments through reduced dependence on conventional banking infrastructure.

- Growth faces its greatest impediment in regulatory ambiguity, with financial institutions reluctant to deploy capital in the absence of explicit guidelines covering licensing, custody requirements and compliance frameworks for digital asset enterprises.

Positioned as one of the Asia-Pacific region's most technologically sophisticated financial markets, Australia now confronts a pivotal decision regarding digital assets and tokenized finance.

A report entitled "Unlocking Australia's $24b Digital Finance Opportunity" was released by the Digital Finance Cooperative Research Centre (DFCRC) alongside the Digital Economy Council of Australia. The document cautions that without rapid modernization of its regulatory architecture, the nation will secure only a minimal fraction of these potential benefits.

According to the report's findings, digital finance and tokenized markets have the capacity to generate approximately A$24 billion (about US$17 billion) in yearly economic advantages for Australia, contingent upon legislative action by lawmakers.

The scale of Australia's digital finance opportunity

Analysis conducted by the DFCRC suggests that digital asset infrastructure and tokenization stand to substantially enhance multiple components of Australia's financial ecosystem. Market efficiency gains, liquidity improvements and expanded investor accessibility are anticipated to generate this economic value.

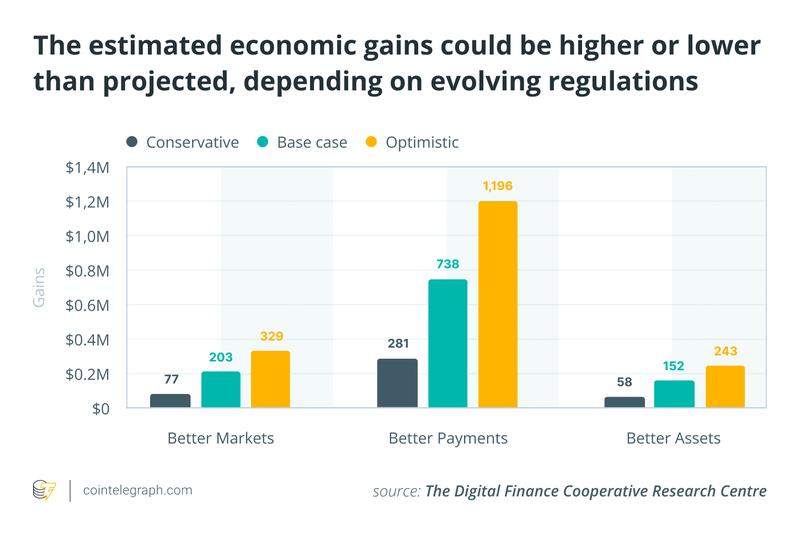

Three primary value sources identified in the report collectively constitute the estimated A$24 billion opportunity.

Improved financial markets

Substantial economic advantages are projected to emerge from tokenized financial markets. Through the registration of conventional securities like stocks or bonds on blockchain-based platforms, markets gain the ability to automate settlement procedures, reduce operational expenses and broaden participation opportunities for investors.

Enhanced transparency and efficiency across a range of assets can be achieved through tokenized infrastructure, including:

- foreign exchange

- investment funds

- public equities

- government debt

Enhanced liquidity combined with improved investor accessibility has the potential to generate increased trading volumes while reducing friction across the financial system.

Improved payments

Various tokenized monetary instruments including stablecoins, bank deposit tokens and central bank digital currencies (CBDCs) possess the capability to accelerate and reduce costs for both local and cross-border payments.

Currently, numerous international payments rely upon correspondent banking networks that frequently prove sluggish and expensive. Payment systems utilizing tokenization could facilitate nearly instantaneous transfers among institutions, compressing settlement timeframes and diminishing transaction costs.

Better use of digital assets

Financial assets gain enhanced programmability and integration capabilities within digital financial services through tokenization. Automated management of tasks like margin calls, collateral administration and settlement becomes possible via smart contracts, replacing processes that currently require manual intervention and consume significant time.

The DFCRC report indicates that nearly fifty percent of asset-related benefits could derive from facilitating novel activities on tokenized infrastructure, encompassing collateralized lending, repo markets and invoice financing.

Did you know? Among the earliest nations to investigate blockchain applications for financial market infrastructure was Australia. The Australian Securities Exchange (ASX) initiated a project in 2017 aimed at replacing its aging clearing system with blockchain technology, though the plan was subsequently reevaluated.

Why regulation is the primary obstacle

Despite considerable promise shown by digital asset markets, the DFCRC report pinpoints regulatory uncertainty as the principal impediment to Australian growth.

Substantial capital investment in emerging technologies is typically avoided by major financial institutions until definitive legal frameworks have been put in place. Absent explicit regulations governing licensing, asset custody and compliance, numerous firms demonstrate reluctance toward launching significant tokenized offerings.

Key structural challenges include:

- Vague licensing: The procedures through which digital asset businesses should secure official permits remain unclear.

- Poor collaboration: Communication channels between industry participants and regulatory authorities are inadequate.

- Limited trials: Practical testing faces constraints due to insufficient large-scale pilot initiatives.

- Legal ambiguity: Tokenized financial products exist in an undefined legal status.

Progress encounters obstacles from these issues despite the availability of requisite technology. Market entry with confidence requires institutional investors to have access to a clearly delineated regulatory foundation.

The high cost of regulatory inaction

Australia's potential gains from digital finance could face severe erosion if modernization of the regulatory framework experiences continued delays.

Should policy stagnation continue unchanged, projections suggest Australia may realize merely A$1 billion (around US$710 million) from tokenized finance and digital assets by 2030. This amount constitutes just a tiny portion of the A$24 billion in achievable benefits possible under more supportive and predictable regulatory conditions.

The magnitude of this shortfall underscores regulatory obstacles' capacity to reshape the trajectory of financial innovation. Without clear, enabling policy frameworks, numerous detrimental outcomes could materialize:

- Pilot initiatives encounter difficulties scaling toward live, production-ready implementations.

- Institutional capital remains uncommitted, avoiding meaningful risk exposure.

- Advanced innovation and skilled talent progressively migrate toward jurisdictions offering regulatory clarity and predictability.

- Australia's domestic financial infrastructure undergoes slower modernization compared to international competitors.

In the final analysis, extended regulatory uncertainty functions not simply as a brake on progress but may actively redirect economic value and opportunities toward nations that have developed favorable digital finance frameworks.

Did you know? One of the Asia-Pacific region's densest crypto ATM networks operates in Australia. Beyond North America, it ranks among the largest markets for cryptocurrency kiosks.

What the industry is asking for in regulation

Initial progress toward establishing a digital asset regulatory framework has been achieved by Australia. Industry stakeholders emphasize, however, that additional measures are essential for unlocking substantial institutional engagement:

- Clear licensing regimes for digital asset platforms: Well-defined licensing pathways are urgently needed for digital asset service providers, exchanges, trading venues and related entities. These encompass precise regulations on permissible operations, operational standards, capital requirements and continuing compliance responsibilities.

- Modern, fit-for-purpose custody rules: Unique risks surrounding security, segregation and operational resilience accompany digital assets. Clear, risk-proportionate custody standards that protect client assets should be established by regulators.

- A coherent framework for stablecoins: Foundational infrastructure for efficient on-chain payments and tokenized markets is widely attributed to stablecoins. Industry participants seek clarification on cross-border regulations, supervision, redemption rights, reserves and issuance to eliminate legal and operational ambiguity.

- Balanced and proportionate consumer and investor protections: Essential safeguards against loss, misconduct and fraud must be implemented. However, careful design is necessary to prevent legitimate innovation from being suppressed.

Addressed collectively, these regulatory components would furnish the clarity financial institutions require before deploying substantial capital and infrastructure toward tokenized finance within Australia.

Why regulatory sandboxes are important

The creation of regulatory sandboxes designed specifically for tokenized financial markets receives recommendation from the DFCRC report.

Testing of novel financial technologies under rigorous regulatory supervision becomes possible for companies through these sandboxes before full licensing is obtained. Regulatory observation of innovation performance in practice occurs through this approach while maintaining controlled risk levels.

An Enhanced Regulatory Sandbox (ERS) under Australian Securities and Investments Commission (ASIC) management already exists in Australia. Eligible firms receive permission to trial specific financial services for restricted periods without holding complete financial services licenses.

Industry groups contend, however, that more specialized sandboxes would accelerate testing and development across critical areas like digital settlement systems and tokenized securities.

Enhanced dialogue between industry participants and regulators would result from targeted sandboxes, empowering policymakers to craft superior regulations grounded in actual testing results.

The role of tokenized government bonds and CBDCs

Essential infrastructure for digital financial markets could be formed through tokenized government bonds and a central bank digital currency (CBDC), according to DFCRC report proposals.

Collateral in financial markets already relies heavily on government bonds. Tokenization would enable automated collateral administration, accelerated settlement and enhanced transparency.

Secure final settlement for tokenized assets could be provided through a CBDC designed for financial institution use rather than public consumption. Combined with bank deposit tokens and stablecoins, it would contribute to constructing a flexible and efficient digital financial transaction system.

The reliable settlement infrastructure institutional markets require for large-scale operation would be created by these instruments.

Did you know? Central bank digital currency trials were experimented with early by Australia's central bank. Previous projects investigated how wholesale CBDC could facilitate automation of bond settlement and other sophisticated financial transactions between institutions.

Project Acacia and Australia's experimentation with digital money

Exploration of these concepts is already underway in Australia through initiatives like Project Acacia. This collaborative effort investigates how digital money could function within tokenized wholesale markets.

Testing of various digital settlement forms, encompassing both CBDCs and stablecoins, occurs within the project to support financial market infrastructure.

Significant roles can be fulfilled by pilot programs of this nature. Testing of technical designs, operational risks and regulatory questions becomes possible for policymakers and financial institutions prior to implementing large-scale systems.

Rule creation by regulators based on practical experience rather than purely theoretical considerations is facilitated through real-world experimentation.

Technological ability alone is not enough

A key conclusion emerging from the DFCRC report establishes that technology by itself proves insufficient for creating new financial markets.

Institutional adoption of tokenized finance requires:

- clear legal frameworks

- reliable settlement infrastructure

- proper custody standards

- effective risk management protocols

- appropriate regulatory oversight

Collectively, these components establish the trust financial institutions need for committing to emerging technologies.

Absent that trust, tokenized finance will likely remain restricted to limited pilot projects instead of integrating into mainstream financial systems.

Australia's competitive challenge

Accelerating global competition to develop digital asset infrastructure is evident. Regulatory frameworks for digital payment systems, stablecoins and tokenized securities are already being constructed by many jurisdictions.

Delays by Australia risk forfeiting talent, investment and innovation to countries providing regulatory clarity more expeditiously.

From this perspective, digital asset regulation transcends mere financial policy concerns. It also constitutes a competitiveness question for Australia's wider economy.

Nations establishing credible digital finance frameworks position themselves advantageously to attract capital and technology firms seeking stable regulatory environments.