Can Strategy's Restructured Capital Plan Eliminate 'Death Spiral' Concerns?

The company's new framework features buyback programs for MSTR and STRC, bolstered cash holdings, and the possibility of Bitcoin liquidation. Can these measures calm mounting "death spiral" anxieties?

As Bitcoin dropped beneath the $60,000 threshold and Strategy's stock declined over 70% from its peak, certain cryptocurrency market participants are asking whether Strategy might mirror Terra/LUNA this market cycle — representing a heavily leveraged wager on crypto infrastructure that collapses when subjected to pressure.

Strategy's answer? A fresh capital structure unveiled Monday designed to calm investor anxieties.

The initiative encompasses buybacks reaching $1 billion for MSTR shares, buybacks totaling $1 billion for STRC and associated instruments, raising STRC's dividend to approximately 12%, and growing the cash cushion to $2.55 billion.

Particularly notable for an organization celebrated for its Bitcoin maximalist philosophy, Strategy additionally indicated willingness to liquidate up to $1.25 billion worth of BTC assets when necessary to satisfy dividend or debt commitments.

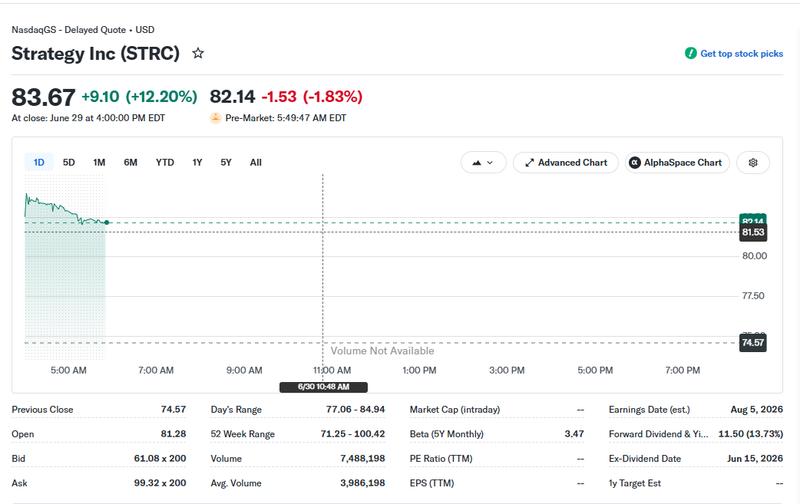

The market reacted favorably to these developments, with STRC and MSTR shares both surging beyond 12% during after-hours sessions. STRC currently sits at $84.86, marking substantial progress from the $72.06 level observed on June 26.

The question remains whether this strategy suffices to calm concerns that STRC's design — reportedly developed by CEO Michael Saylor utilizing an LLM — might leave Strategy vulnerable to a "death spiral" characterized by reflexive financing hazards during turbulent market periods?

Understanding STRC and its contentious nature

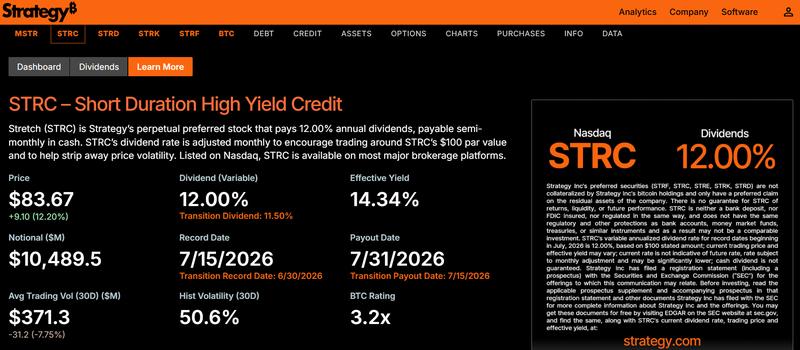

STRC forms part of Strategy's capital architecture tied to its comprehensive Bitcoin treasury approach. The instrument occupies a middle ground between conventional equity and debt-style securities, delivering yield to investors while preserving connection to the firm's Bitcoin portfolio.

Strategy characterizes STRC as perpetual preferred equity issuing a 12% yearly dividend based on a $100 par value, financed through its cash holdings and Bitcoin-connected capital structure.

Though the instrument aims to deliver financing adaptability without traditional debt issuance, market observers have raised questions about whether its resilience hinges on sustained investor interest in secondary trading venues, especially during Bitcoin price swings or constrained liquidity environments.

In contrast, Strategy's ordinary shares are designated MSTR and signify equity ownership in Strategy accompanied by shareholder voting privileges. The trajectories of these two instruments are tightly connected, though they remain distinct. Likewise, Strategy's status as Bitcoin's largest institutional purchaser (and potentially a future seller) means its fortunes are presently deeply connected with Bitcoin's market value.

Persistent gold advocate and Bitcoin skeptic Peter Schiff has continually criticized Strategy's approach, highlighting that it "can't sell Bitcoin without crashing the price of Bitcoin. Even if Strategy merely stops buying Bitcoin, that change alone would crush the market."

Nevertheless, Taran Dhillon, head of digital assets at Kula, informed Cointelegraph that "Bitcoin volatility alone is unlikely to break a structure like Strategy's."

He explained that a more significant challenge is "whether Bitcoin remains under pressure while access to capital becomes progressively more expensive or difficult."

The pessimistic perspective: reflexive mechanisms and liquidity reliance

Critics contend that Strategy's complete fundraising and stock framework is fundamentally reflexive, magnifying both ascending and descending market cycles. The identical mechanism that magnifies profits during bull runs can hasten deterioration throughout bear markets, when declining Bitcoin and equity valuations converge with diminished demand.

Ripple CEO Brad Garlinghouse articulated precisely that position on CNBC recently. "Financial engineering does not drive long term value," he stated.

Kyle Rodda, senior analyst at Capital.com, informed Cointelegraph that Strategy essentially functions as a momentum-fueled Bitcoin acquisition mechanism, wherein capital generation finances Bitcoin acquisitions that, consequently, bolster the organization's valuation. Nevertheless, he cautioned that this dynamic can invert during stressful conditions.

"Strategy's business definitely compounds momentum in both directions," Rodda explained, noting that under adverse circumstances, escalating financing expenses and deteriorating investor enthusiasm can strengthen downward forces.

He further contended that secondary market liquidity represents a structural requirement, suggesting large-scale liquidations or refinancing strains could generate broader repercussions within Bitcoin markets directly.

Within the Bitcoin community, Charles Edwards, the founder of Capriole Investments, stands among Strategy's most critical recent observers.

He drew parallels between stressed circumstances in digital asset treasury firms and wider crypto deleveraging episodes, cautioning that reflexive mechanisms can intensify losses when leverage and market sentiment worsen.

"Anyone else getting LUNA 2022 vibes on MicroStrategy?" he wrote on June 26.

The balanced perspective: genuine risk lies in funding markets, not Bitcoin

Despite bearish commentary regarding Strategy accumulating on X, Dhillon informed Cointelegraph that pressure would probably first manifest in funding circumstances, identifying expanding discounts, elevated yields, and diminished issuance capability as preliminary warning indicators.

From his perspective, Strategy's Bitcoin reserves matter less than whether the organization can sustain refinancing or capital rotation effectively during market stress periods.

And although STRC's inability to preserve its "peg" at $100 has generated considerable alarm, STRC isn't pegged to $100 similarly to how stablecoins peg to $1. The yield simply becomes more appealing as the price descends below $100, which theoretically, ought to attract purchasers who push pricing back toward $100 eventually.

A Bitfire Research analysis shared with Cointelegraph stated that STRC's recent price disruptions shouldn't be viewed as structural breakdown.

The research firm maintained that de-pegging occurrences are predominantly influenced by sentiment and liquidity circumstances rather than modifications to Strategy's core fundamentals or financial health profile.

"Strategy (formerly MicroStrategy) faces no near-term insolvency risk."

Bitfire Research

Optimistic perspective: stress doesn't equal insolvency

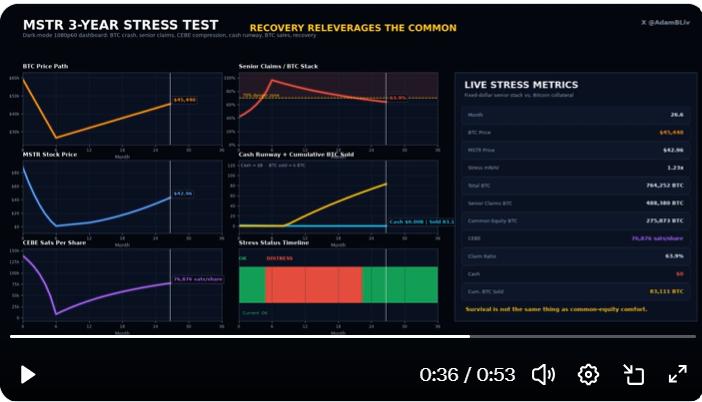

Strategy advocate Adam Livingston, a Bitcoin proponent and writer, conducted what he characterized as a "three-year MSTR stress test" under extreme scenarios, encompassing a 55% Bitcoin decline, frozen capital markets, and persistent cash depletion requiring substantial Bitcoin liquidations to fulfill commitments.

Within his framework, Strategy's senior obligations grow dramatically in Bitcoin denominations, while the organization's "common equity Bitcoin exposure" (CEBE) contracts substantially. He characterized this as "CEBE getting annihilated", declining from 138,161 sats per share to 7,884 sats per share at the simulation's lowest point.

The framework assumes zero fresh Bitcoin acquisitions or equity offerings throughout the decline, with roughly 115,727 BTC liquidated across three years to cover commitments before stabilization circumstances emerge.

Notwithstanding the drawdown's intensity, Livingston's framework ultimately demonstrates Strategy persisting through the cycle, concluding with above 700,000 BTC retained on its financial statements and a recovering net asset position once market circumstances stabilize.

Strategy's actual modifications

The new structure signifies Strategy's most direct effort to date addressing liquidity and reflexivity risk concerns.

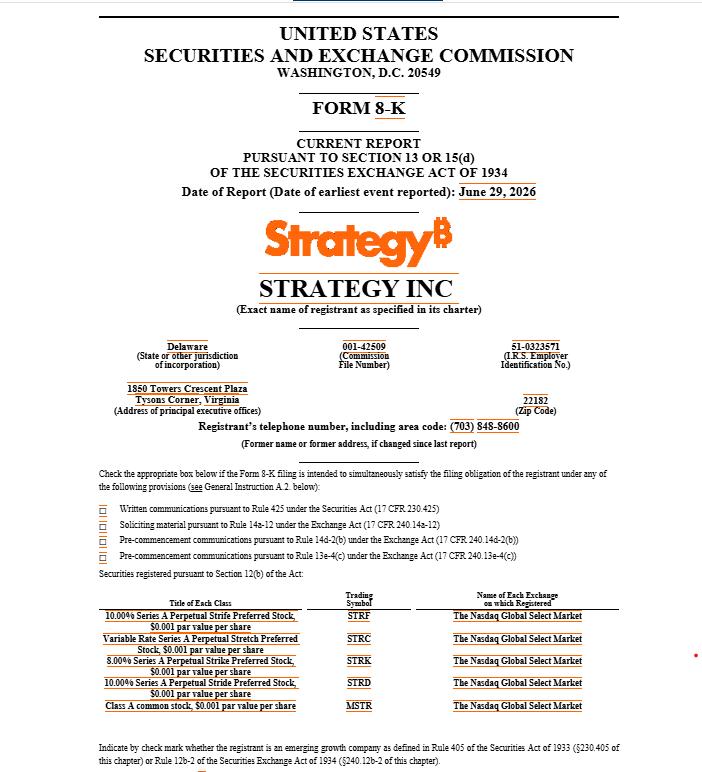

Principal elements of Strategy's June 29 8-K submission that seek to rebuild market confidence in the organization, include repurchase programs for MSTR equity and STRC and substantial emphasis on growing cash holdings to fund dividend payments. The final resort option of liquidating up to $1.25 billion in Bitcoin assets to cover dividends is incorporated partially as a method to convince markets Bitcoin maximalist Michael Saylor will grudgingly liquidate holdings if circumstances demand it.

Dhillon stated the structure "meaningfully improves" clarity regarding how Strategy would react under duress, with the enhanced $2.55 billion reserve and more transparent Bitcoin monetization approach helping reinforce investor trust.

However, Schiff highlighted that MSTR's present market capitalization stands at $30 billion, whereas its Bitcoin holdings currently value $50 billion. "Until MSTR's market cap rises above the value of its Bitcoin, any Bitcoin bought by issuing MSTR shares creates a negative Bitcoin yield," he explained.

Enhanced capabilities, identical fundamental wager

Although the structure bolsters Strategy's capacity to navigate immediate-term pressure, it doesn't remove its dependence on capital markets to maintain its wider Bitcoin accumulation approach.

As Dhillon conveyed to Cointelegraph, the critical examination will be whether funding circumstances stay available during market stress intervals, rather than Bitcoin price movements exclusively.

He noted that the revision clarifies Strategy's capital distribution methodology, and provides management a more explicit sequence of actions, which renders its comprehensive approach more believable.

For skeptics like Rodda, the fundamental anxiety remains. Strategy's architecture stays vulnerable to reflexive mechanisms if liquidity contracts across both stock and credit venues.

While Strategy's initiative introduces more transparent liquidity reserves, repurchase programs, and backup alternatives, including prospective Bitcoin liquidations, the discussion surrounding structural reflexivity hasn't been completely settled.

The current question is not whether STRC is inherently vulnerable theoretically, but whether Strategy's broadened capabilities can endure an extended interval of capital market pressure, and whether investors continue seeking exposure to an instrument that magnifies Bitcoin's fluctuations and introduces risk, instead of merely following them.