Staking Revenue Takes Center Stage for Ethereum Treasury Companies Amid ETF Competition: Analysis

According to Everstake's analysis, staking revenue represented 60% of publicly disclosed income across six companies holding Ethereum treasuries, as loss-reporting firms accumulated $1.41 billion in combined losses.

Companies maintaining Ethereum treasuries face mounting pressure to drive income through staking and alternative yield-generating strategies as the emergence of spot cryptocurrency exchange-traded funds (ETFs) diminishes the value proposition of publicly traded firms that merely hold Ether (ETH), a recent Everstake analysis reveals.

Revenue from staking represented approximately 60% of total disclosed income on average across six ETH treasury companies that reported staking-specific earnings separately, according to findings from the staking infrastructure provider.

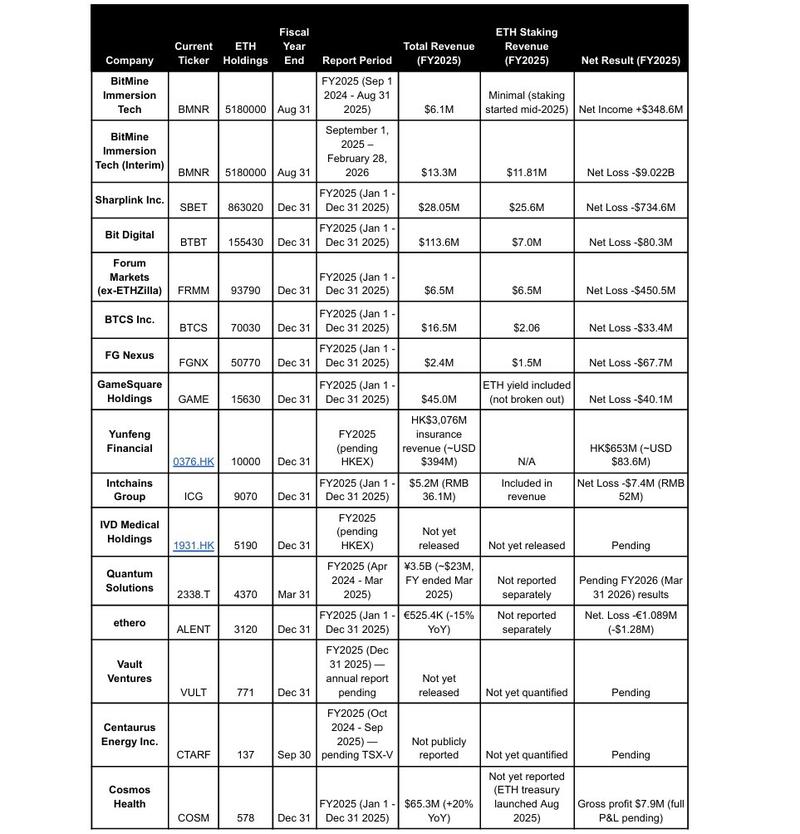

The analysis conducted by Everstake examined 15 publicly traded companies employing ETH treasury strategies and discovered that firms within its research sample reporting 2025 losses accumulated approximately $1.41 billion in aggregate net losses. In a separate finding, BitMine Immersion Technologies disclosed a $9.02 billion net loss for the six-month period concluding Feb. 28, although this figure primarily reflected unrealized losses on digital asset holdings rather than operational losses, the analysis noted.

The 60% figure representing staking revenue was calculated based on six companies that provided separate disclosure of staking-related income: BitMine Immersion Technologies, SharpLink, Bit Digital, Forum Markets, BTCS and FG Nexus. Companies failing to itemize stakeholder-related rewards or those with outstanding annual results were not included in the calculation.

The analysis characterizes this transition as an element of a wider revaluation of digital asset treasury companies (DATs), which historically provided among the limited regulated mechanisms for public-market investors to obtain cryptocurrency exposure. Everstake contends that spot ETFs have diminished the passive-exposure premium previously enjoyed by DATs, compelling treasury companies to defend their valuations through staking, DeFi lending, MEV capture and additional yield-generation tactics.

"DATs that rely on passive exposure are being structurally repriced," Everstake co-founder Bohdan Opryshko said in the report. He added that deployment is "no longer limited to standard protocol staking" and now includes liquid staking, DeFi lending and validator-level strategies.

Speaking with Cointelegraph, Opryshko clarified that the research does not suggest staking revenue by itself can sustain every ETH treasury business model or neutralize all associated risks. Fluctuations in ETH pricing, dilution effects, discounts to net asset value, financing expenses and operational costs can still exceed staking yields, especially for companies operating with fragile capital structures or suboptimal treasury management practices, he explained.

He said the report's point is narrower: "Passive ETH accumulation is becoming harder to justify as a standalone public-market strategy, particularly after spot crypto ETFs gave investors cleaner access to passive exposure."

Within this landscape, staking and other approaches to active asset deployment may prove "necessary, though not sufficient," for ETH treasury companies seeking to maintain viable business models, he continued.

ETFs matter, but may not be the only pressure point

Ignacio Aguirre, the chief marketing officer at crypto exchange Bitget, said spot ETFs have made it harder for ETH treasury companies to justify a premium based on ETH exposure alone. However, he cautioned against attributing the repricing entirely to ETFs.

"I would not over-attribute it to spot ETFs alone," Aguirre told Cointelegraph. He said ETH treasury companies are still equity vehicles, meaning investors also weigh ETH price performance, balance sheet quality, dilution risk, treasury strategy, execution and broader market sentiment.

According to Aguirre, staking has the potential to enhance the ETH treasury business model by establishing a recurring income stream, although its effectiveness hinges on whether the generated yield proves substantial enough to counterbalance operational expenses, dilution effects and price volatility.

He further noted that staking-enabled ETH ETFs could emerge as an additional pressure point for treasury companies in the future, but characterized them as "more complementary than existential threats."