Five Asset Categories Leading the Rapid Onchain Tokenization Revolution

From government treasuries and real estate to equities, commodities, and private credit, Real World Assets are being tokenized at unprecedented rates. While still relatively modest compared to traditional finance, this sector is experiencing explosive growth.

In a recent research publication, Geoff Kendrick, who leads digital assets research at Standard Chartered, forecasted that DeFi could see assets totaling $2.7 trillion by the year 2030.

According to his analysis, a mere 3% of stablecoins and 10% of tokenized real-world assets (RWAs) currently participate in DeFi activities. His projection, however, suggests this figure will climb to 30% within the next six years.

Such growth would represent a multiplication by 37 times compared to current levels, and the accelerating pace of tokenization provides Kendrick with grounds for this bullish perspective.

By the conclusion of June, the tokenized real-world assets market — encompassing equities, bonds, property, precious metals, and carbon credits — achieved $32.22 billion in distributed on-chain value. This represents nearly triple the approximately $11.8 billion RWA market recorded twelve months prior. When stablecoins, essentially tokenized representations of real world fiat currencies, are included in these calculations, the comprehensive tokenized market exceeds $328.8 billion.

The number of total RWA asset holders has expanded to 937,928, reflecting a 13% increase in the previous month alone, based on data compiled by RWA.xyz.

What follows is a detailed examination of the specific drivers propelling expansion throughout various RWA verticals.

US Treasuries

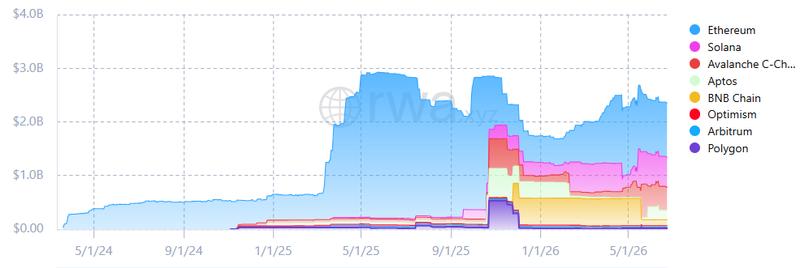

Government-issued US Treasury bills, notes, and bonds constitute the most substantial tokenized asset category measured by on-chain value, standing at $15 billion. These instruments offer familiarity for market participants, present minimal risk profiles, maintain high liquidity and produce yields — capabilities that stablecoins have yet to deliver.

Introduced in March 2024, Blackrock's BUIDL fund achieved over $2.9 billion in total asset value by June 2025. Its current position stands at $2.23 billion following some capital reallocation and inter-platform competition. The fund has paid out more than $100 million in dividends and maintains operations across Ethereum, Solana, Polygon, Avalanche, Arbitrum, Optimism, Aptos, and BNB Chain.

During February 2026, Uniswap Labs partnered with Securitize to announce that BUIDL shares became accessible for trading on UniswapX. This development placed a significant, regulated, institutional tokenized fund onto a decentralized exchange (though with limitations regarding eligible buyers and sellers).

This is the unlock we've been working toward: bringing the trust and regulatory standards of traditional finance to the speed and openness for which DeFi is known.

Carlos Domingo, CEO of Securitize

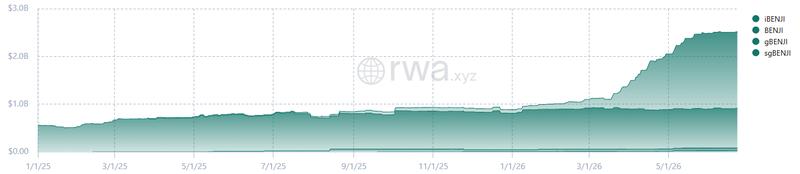

A comparable offering comes from Franklin Templeton's OnChain US Government Money Fund, tokenized as BENJI. This product has grown to $2.44 billion and operates across Avalanche, Arbitrum, Aptos, Base, and BNB Chain, Stellar, Ethereum, Solana, Polygon.

Additional notable Treasury offerings consist of Circle's USYC ($3.1 billion), Ondo's product suite ($3.7 billion) and WisdomTree's WTGXX ($764 million).

Private Credit

Private credit — financing that gets issued, negotiated and maintained by institutions outside the traditional banking system — represents another rapidly expanding category among RWAs.

The attraction parallels that of Treasuries, though private credit delivers superior yields compared to government obligations. Additionally, tokenization introduces liquidity to the private credit space, an area notorious for multi-year capital commitment periods.

Today, a corporate treasurer or investment manager can maintain private credit holdings that are transferable on-chain, deployable as collateral, and redeemable on demand.

The dominant platforms for tokenized private credit issuance are Maple Finance and Stokr. Both command approximately 22% of the market respectively, per RWA.xyz data. The aggregate value of tokenized private credit stands at roughly $6.2 billion.

Stocks and ETFs

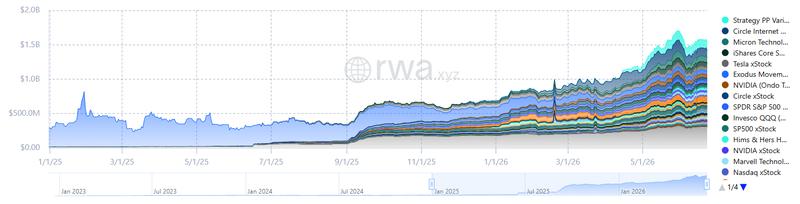

At present, equities comprise a relatively small fraction of total tokenized assets at just $2.19 billion, according to RWA.xyz. This figure has risen by nearly 50% over merely the last thirty days, indicating exceptionally rapid growth, with a significant expansion anticipated in the near term.

Last May, the Depository Trust & Clearing Corporation (DTCC) revealed intentions to pilot tokenized securities trading. DTCC handles clearing and settlement for virtually all US equity transactions and maintains custody of over $114 trillion in securities.

These pilot programs are scheduled to commence this month, with a potential full commercial rollout by October.

The pilot assets encompass Russell 1000 equities, leading index ETFs, and US Treasuries. Over 50 financial institutions are taking part, including BlackRock, Goldman Sachs, JPMorgan, Citigroup, Bank of America, Morgan Stanley, Circle, Ondo Finance, and Ripple Prime.

Ondo Finance currently controls approximately 60% of the tokenized equity marketplace via its Global Markets platform. During March 2026 the company established a partnership with Franklin Templeton to tokenize five ETFs.

The following month saw another partnership form with Broadridge Financial Solutions, enabling tokenized stock and ETF holders to submit voting preferences for their underlying shares.

Gold and commodities

Tokenized gold, representing the largest subsection within tokenized commodities, has existed for several years, though 2026 provided it with an unanticipated stress test.

As US–Iran tensions intensified in early 2026, conventional markets had closed for the day. Tokenized oil and gold markets remained operational.

Following US and Israeli attacks on Iran earlier this year, Wall Street trading operations found themselves increasingly relying on on-chain perpetual futures platforms as their sole available venue for pricing gold, oil, and additional risk-off assets outside regular trading hours.

Weekend trading volumes on on-chain commodity perpetuals have surged ninefold since early 2026. Onchain perpetual futures for commodities currently constitute over 67% of builder-deployed contracts on decentralized exchanges.

The key insight is that tokenized commodities, operating on continuously open markets, deliver genuine advantages during geopolitical crises, which operate independently of traditional market schedules.

Tokenized commodities reached $5.8 billion during March 2026 and have since retracted to $4.7 billion presently, with gold comprising a substantial majority of that total.

Trading volumes for tokenized gold have progressively begun moving in correlation with traditional gold markets. This relationship was historically weak but surpassed the 0.70 threshold during Q1 2026, indicating the onchain market is reaching maturity.

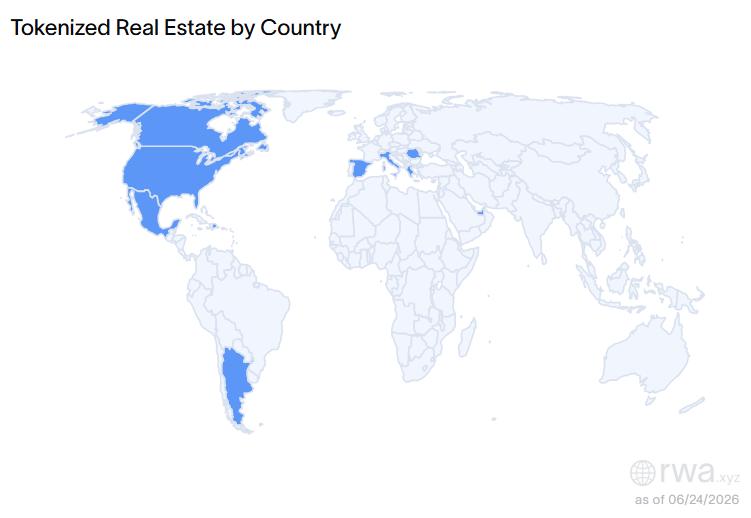

Real estate

Real estate tokenization has represented more of an aspirational concept to date rather than a reality achieved at meaningful scale.

As a segment of the RWA ecosystem, real estate accounts for merely $202.7 million in assets currently, though this figure is poised for growth with its introduction into several major, regulated markets during the current year.

Dubai's Land Department initiated the second phase of its real estate tokenization initiative in February 2026, making tokenized property units available for resale transactions. Hong Kong's Securities and Futures Commission similarly granted approval for real estate tokenization products from Derlin Holdings during the identical quarter.

Real estate tokenization provides fractional ownership opportunities to investors lacking sufficient capital for traditional real estate investment entry points. Each token signifies a share of the property, potentially offering proportional rental income and the capability to trade positions without awaiting a complete property sale.

RWAs are still relatively small

Tokenized real-world assets are experiencing growth, though considerable room for expansion remains. Tokenized Treasury products constitute the largest and most developed category of RWAs, representing nearly $15 billion. This total remains dwarfed by the conventional US Treasury market of approximately $30 trillion.

Tokenized equities represent a negligible fraction compared to the DTCC's $114 trillion in assets under custody.

Liquidity remains relatively limited as well, with numerous RWAs experiencing minimal secondary market trading and extended holding durations.

However, regulatory bodies are starting to provide support. During March, the SEC granted approval to a Nasdaq proposal permitting certain equities to be traded and settled through tokens. Market analysts and industry observers anticipate broader approval for stock token trading in the immediate future, with SEC Chair Paul Atkins expected to authorize RWAs via an "innovation exemption."

The question now appears to no longer be whether real-world assets will be tokenized, but how quickly.