Tech Stock and Bitcoin Correlation Exaggerated, Says NYDIG Analysis

According to NYDIG's Greg Cipolaro, the perceived convergence between Bitcoin and technology stocks is overstated, with both assets simply responding to broader macroeconomic factors instead of genuinely moving in sync.

The simultaneous upward movement of Bitcoin and United States software equities represents shared sensitivity to macroeconomic developments rather than any fundamental alignment, according to an analysis from financial services firm NYDIG.

Over the previous week, Bitcoin (BTC) experienced gains alongside software stocks in the United States, prompting numerous observers to suggest the digital currency functions as a stand-in for the technology sector, noted Greg Cipolaro, NYDIG's research director, in a Friday memo.

"Although their indexed pricing shows a visually persuasive alignment, the interpretation that Bitcoin and software equities have undergone structural convergence, or that they possess comparable vulnerability to factors like AI or quantum computing threats, is overemphasized," he stated.

Cipolaro further explained that the synchronized price movement "more credibly represents common vulnerability to the prevailing macroeconomic environment, particularly long-duration, liquidity-dependent risk assets, as opposed to demonstrating a fundamental convergence linking Bitcoin with software equities."

Equity markets don't fully explain Bitcoin's price action

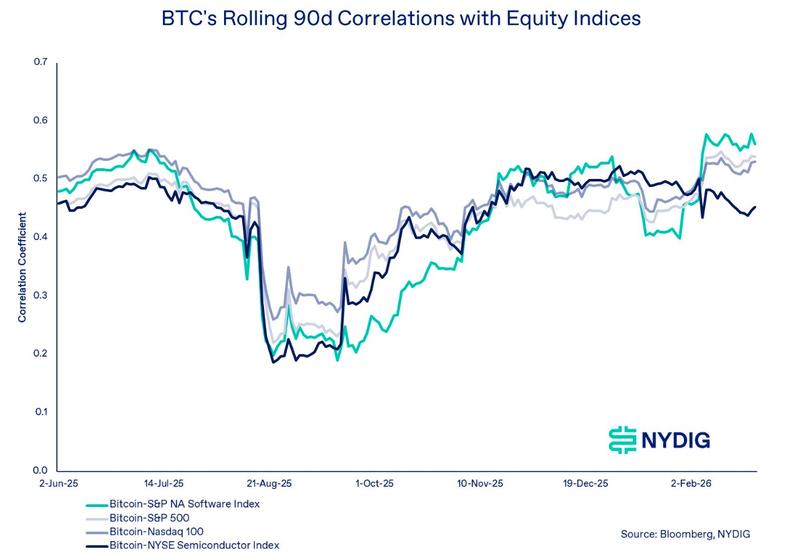

While Bitcoin's association with software equities has strengthened on a 90-day rolling measurement since reaching its record peak above $126,000 in early October, Cipolaro noted that its relationships with both the S&P 500 and Nasdaq have similarly intensified recently, suggesting that "this shift is not exclusive to software equities."

Despite these elevated correlations between Bitcoin and software stocks as well as the major indices, "the bulk of Bitcoin's price action continues to be unexplained by equity performance," Cipolaro emphasized.

From a statistical perspective, he explained that merely one-quarter of Bitcoin's price fluctuations can be attributed to stock market correlation, while no less than 75% of its variations stem from factors independent of conventional equity benchmarks.

According to Cipolaro, it seems Bitcoin is not receiving valuations as a protective instrument against macroeconomic uncertainty, which accounts for "the persistent disappointment surrounding Bitcoin's inability to 'behave like gold' notwithstanding the digital gold characterization."

He further observed that market participants seem to be distributing capital across a risk spectrum, instead of acquiring Bitcoin based on a "distinctive monetary argument."

Nevertheless, Cipolaro maintained that Bitcoin possesses unique market characteristics and economic catalysts, highlighting its blockchain network usage and expanding adoption patterns, coupled with regulatory and governmental policy changes that distinguish it from alternative investments.

"This differentiation validates bitcoin's function as a portfolio diversification tool," he explained. "Although cross-asset correlations with equities are presently heightened, they continue to fall well short of being decisive factors in bitcoin's performance."