From Dot-Com Disaster to Bitcoin Kingpin: Is MicroStrategy's Past Coming Back to Haunt It?

After imploding spectacularly in the dot-com bubble, Michael Saylor reinvented MicroStrategy as the planet's biggest corporate Bitcoin holder. Has he truly changed, or are old patterns emerging?

During March 2000, Strategy's executive chairman Michael Saylor witnessed over $6 billion evaporate from his personal wealth within the span of just 24 hours.

The stock price of MicroStrategy had cratered by over 60%, catapulting the thirty-five year old tech mogul into the epicenter of the infamous dot-com implosion.

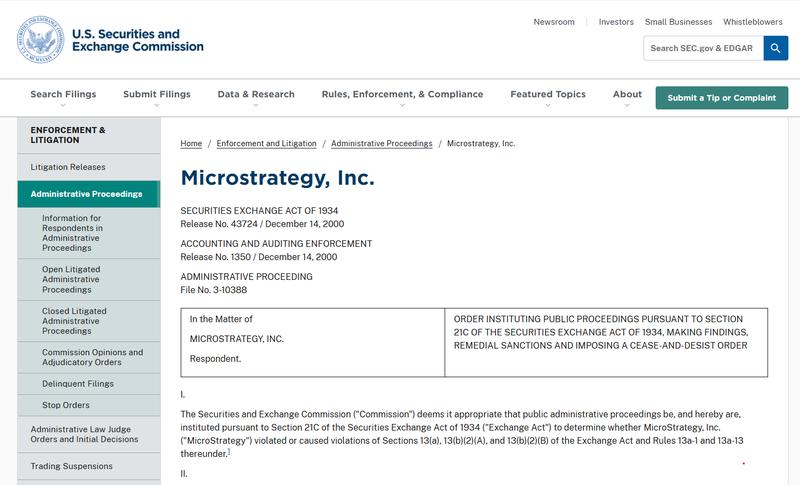

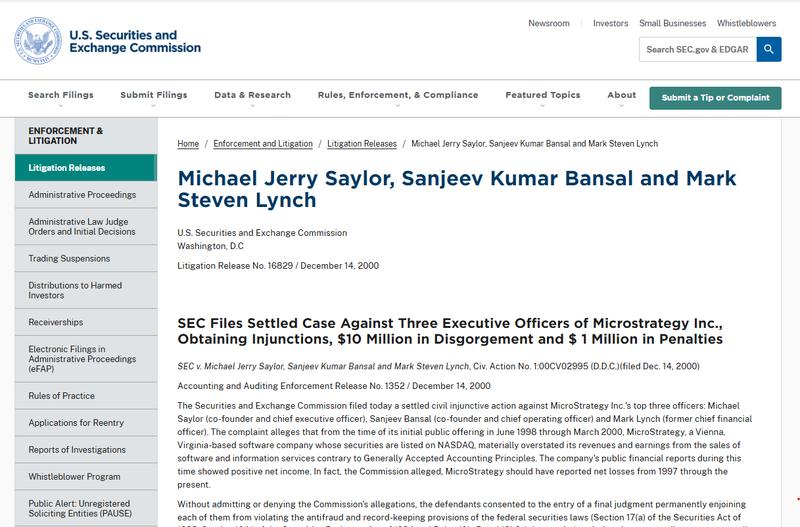

The firm subsequently reached a settlement with the US Securities and Exchange Commission regarding civil fraud allegations related to how it handled accounting matters, though it neither confirmed nor refuted any culpability. While MicroStrategy wasn't responsible for triggering the dot-com bubble's collapse, this dramatic episode ranked among the most prominent corporate disasters of that time period, transforming the company into an emblem of the era's financial recklessness and hazards.

Fast forward more than 25 years, and the unwavering Bitcoin advocate finds himself once more at the nucleus of one of the most intensely scrutinized financial ventures on Wall Street.

The enterprise, which has since rebranded to simply Strategy, currently possesses 843,775 Bitcoin, surpassing every other publicly traded corporation. Its approach has motivated dozens of other listed companies to implement Bitcoin treasury strategies modeled after its own.

However, Strategy has evolved beyond merely stockpiling Bitcoin, having created a complex array of financial engineering tactics that create division among investors and market analysts. Certain observers interpret it as an advanced corporate treasury approach that's virtually foolproof, whereas others contend that the company is accumulating layers of escalating risk.

"The discussion evolves beyond merely buying Bitcoin to encompass how these holdings are financed, overseen and, if required, liquidated or converted to cash," Drew Forman, senior vice president and head of strategy at Talos, explained to Cointelegraph.

Transitioning from acquisition to oversight

On June 29, Strategy introduced a novel capital structure that permits the company to liquidate Bitcoin for funding preferred stock dividend payments, strengthening its cash position and buying back securities.

For an organization that had devoted over five years emphasizing that its Bitcoin holdings were meant for accumulation, not liquidation, this shift triggered considerable concern.

Just days afterward, Strategy revealed the liquidation of 3,588 Bitcoin, marking its most substantial sell-off since embracing BTC as its core treasury reserve asset in 2020.

In the eyes of Strategy supporters, these modifications demonstrate the organic progression of an organization overseeing a Bitcoin treasury worth billions of dollars, as opposed to representing a dramatic reversal.

Conversely, detractors contend that Strategy's increasing dependence on preferred stock instruments, dividend responsibilities and third-party financing has rendered the framework more convoluted and interconnected, rather than strengthening its stability.

The journey that led MicroStrategy to Bitcoin

MicroStrategy stood among the most rapidly expanding software enterprises during the 1990s internet explosion, delivering business intelligence software solutions to prestigious customers such as McDonald's, Nike and eBay, elevating Saylor to the ranks of America's wealthiest business leaders.

However, on March 20, 2000, this upward trajectory abruptly stalled when MicroStrategy disclosed the necessity to revise its financial statements for fiscal years 1998 and 1999 because of accounting discrepancies.

The firm's shares went into freefall, plunging from $260 per share down to merely $86 during one trading session. The decline persisted throughout subsequent weeks. By April 13, following MicroStrategy's announcement that it would additionally need to restate its 1997 financial statements, shares settled at $33 per share.

While that incident might have permanently tarnished many corporate leaders' reputations, Saylor dedicated the following twenty years to reconstructing the enterprise primarily away from public attention until summer 2020, when MicroStrategy declared its intention to establish Bitcoin as its principal treasury reserve asset, with Saylor emerging as cryptocurrency's most outspoken proponent.

He compared maintaining cash reserves amid an era of extraordinary pandemic-era monetary stimulus to grasping "a melting ice cube." On August 11, the company executed its initial $250 million Bitcoin acquisition.

During that period, very few publicly traded corporations maintained Bitcoin within their balance sheets, and this strategic move was predominantly perceived as a dangerous gamble rather than a template for corporate financial management.

However, Bitcoin's valuation shortly commenced a steep ascent, fueled by the abundance of available liquidity, and Strategy's market capitalization expanded dramatically. Almost overnight, Saylor's disputed choice appeared more akin to brilliant foresight and the enterprise rapidly transformed into a leveraged vehicle for Bitcoin exposure on Wall Street.

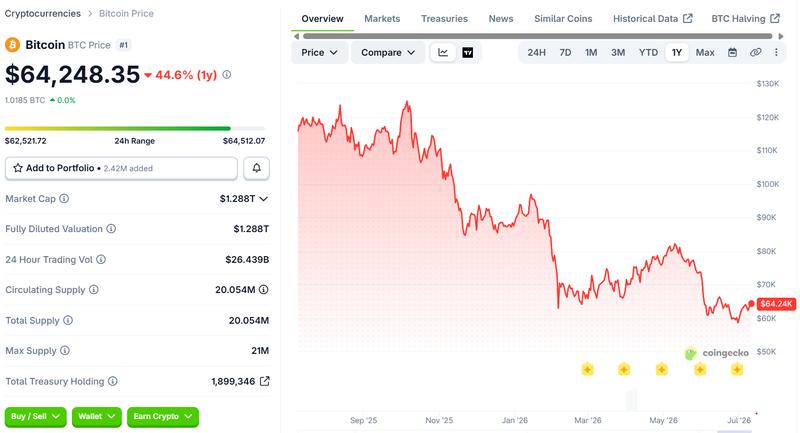

Numerous publicly listed companies embraced modified versions of its treasury approach, and presently, Strategy's Bitcoin reserves are valued at over $54 billion. Yet with BTC trading considerably below its all-time peak above $126,000 reached in October 2025, the company's Bitcoin gambit has faced repeated scrutiny.

Critics maintain that Strategy's framework functions exclusively if Bitcoin continues rising in value and investors keep supplying fresh capital. Certain analysts have even cautioned that, during extended market downturns, these underlying mechanics could trigger what's known as a death spiral within Strategy's financial architecture.

Different mechanism, same problem

Whether Strategy exemplifies a groundbreaking transformation or simply history coming full circle depends primarily on investors' risk interpretation.

For certain critics, the parallels with 2000 aren't centered on accounting irregularities but rather Saylor's propensity to construct his enterprise around a high-stakes corporate framework that virtually no other chief executives would seriously consider.

"Saylor is insane (not an insult, just a diagnosis) and is either a fool or a knave," Aswath Damodaran, professor of finance at NYU Stern School of Business, told Cointelegraph in an email.

"It hurts my brain cells just thinking about MSTR and I don't have enough to waste on it."

David Trainer, chief executive of investment research firm New Constructs, likewise maintains a critical perspective. He contended that although today's Strategy bears little resemblance to the organization that imploded during the dot-com crash, investors are nonetheless being asked to invest exceptional confidence in Saylor's most recent corporate venture.

"Different mechanism, same underlying problem: the equity is a leveraged wrapper around a volatile asset, with no fundamental earnings power supporting the valuation," he said.

He explained that the dot-com catastrophe stemmed from inaccurate financial disclosure. The SEC alleged in 2000 the company's financial statements had "showed positive net income" when it should have "should have reported net losses from 1997 through the present." Though Saylor and two executives consented to pay a $10 million fine to resolve the matter, they didn't acknowledge responsibility for any of the SEC's accusations.

"That was a [...] mismanagement risk layered on a real (if over-hyped) software business," he said.

Presently, the organization's financial records are "cleaner," he maintained, with the hazards now embedded within a capital framework constructed around financing increasingly substantial Bitcoin acquisitions rather than software development.

Strategy currently operates with a "large and growing balance of convertible debt and perpetual preferred stock," he noted, highlighting the $6.7 billion in convertible notes and $15.5 billion in preferred stock outstanding as of late May 2026, utilized exclusively to purchase additional Bitcoin.

"The software business is now a rounding error next to the balance sheet," he said.

In Trainer's view, the more significant worry isn't Bitcoin itself, but rather the premium that investors are prepared to pay for gaining exposure through Strategy. Should that premium vanish, one of the firm's fundamental competitive advantages evaporates alongside it.

"Once you're structurally reliant on issuance and issuance becomes value-destructive, the company has to either sell Bitcoin, take on more expensive financing or simply stop growing," Trainer said.

Treasury management, not just HODLing

Forman suggested that investors ought to concentrate on how the organization handles its progressively sophisticated corporate treasury approach.

"Strategy's position can't be understood simply by looking at the size of its Bitcoin holdings," Forman told Cointelegraph.

He indicated that Strategy's readiness to liquidate Bitcoin represents less of a deviation from Saylor's longstanding accumulation philosophy than a practical necessity of operating a corporate balance sheet. "I see it as a pragmatic evolution of a more complex treasury strategy," he said.

"The broader takeaway is that Bitcoin is increasingly being treated as an institutional asset class," he added, emphasizing that instead of merely determining whether to acquire Bitcoin, corporations will progressively need to contemplate governance, liquidity management, execution and risk management.

So, has Saylor rewritten his legacy?

26 years after MicroStrategy's accounting scandal, the questions surrounding Strategy have changed.

Few critics question the integrity of the company's financial reporting, but whether its increasingly complex Bitcoin strategy can endure prolonged market stress.

Saylor has fundamentally changed the way many public companies think about corporate treasuries, and many have followed his lead.

But whether Saylor has rewritten his legacy won't be decided by the next bull run, but on how well Strategy performs if the markets continue to turn against it.

Cointelegraph reached out to Strategy but did not receive a response. A spokesperson from the SEC declined to comment on the settlement case.