Capital efficiency takes a hit from crypto's real-time settlement model: Buchman

The cryptocurrency industry's focus on immediate settlement comes with a significant trade-off in capital efficiency, requiring excessive collateralization and creating barriers to market expansion, according to Cosmos co-founder Ethan Buchman.

The cryptocurrency sector's drive toward immediate settlement has introduced a significant capital inefficiency challenge, compelling trading entities to fully finance each individual transaction and sparking questions about the market's ability to handle increased trading volumes as the industry expands.

What this means in practical application is that trading entities find themselves unable to net their payables against their receivables, resulting in the movement of substantially more capital than would otherwise be required to complete trade settlements.

According to Ethan Buchman, the founder of Cycles Protocol and a co-founder of Cosmos, the cryptocurrency markets suffer from being "asset-brained." His perspective is that the industry approaches the financial ecosystem as though it were a worldwide equity market where value undergoes constant movement and exchange.

But that misses the whole other side of the balance sheet, which is liabilities, and every movement of assets is in service of discharging a liability.

Ethan Buchman told Cointelegraph

The cryptocurrency industry has optimized its infrastructure for immediate settlement, eliminating the batching and netting mechanisms that enable traditional financial systems to preserve liquidity. This design choice at the foundational layer generates pressure to reintroduce clearing mechanisms if the sector is to achieve greater scale.

The logic behind TradFi's delayed settlement

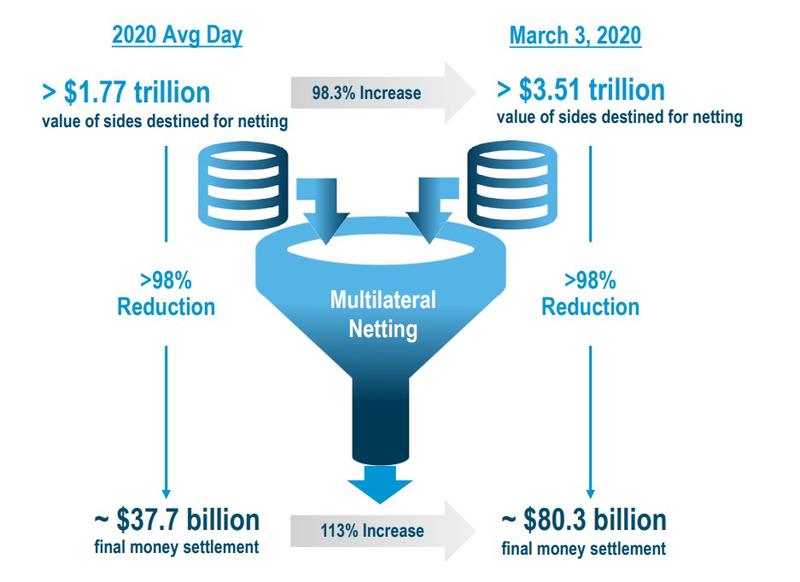

The clearing process involves reconciling and netting participant obligations prior to settlement, which enables participants to offset their payables against their receivables, ensuring that only the net difference requires movement.

To illustrate, if Alice has an obligation to pay Bob $100 while Bob simultaneously owes Alice $90, the clearing process means Alice transfers only $10 rather than processing the complete amounts in both directions.

Within traditional financial infrastructure, settlement delays provide the necessary window to batch and net multiple trades before executing final payment.

A lot of people look at T+2 settlement and think it's inefficient and should be instant — that misses the point. Some of that delay exists to give time for batching and clearing.

Buchman said

At institutional scale, this occurs through clearinghouses such as the Depository Trust & Clearing Corporation, which function as central counterparties responsible for netting obligations and administering settlement risk. The outcome is that financial infrastructures can consolidate substantial transaction volumes into significantly smaller net flows.

Prior to the establishment of central banking systems, merchants conducting business at European trade fairs would settle their debts through netting obligations across multiple parties, which minimized the requirement to transport physical currency. Through time, these commercial practices transformed into more structured clearing systems.

Buchman also referenced subsequent experiments conducted in Yugoslavia and Slovenia as illustrations of multilateral netting implemented at institutional scale.

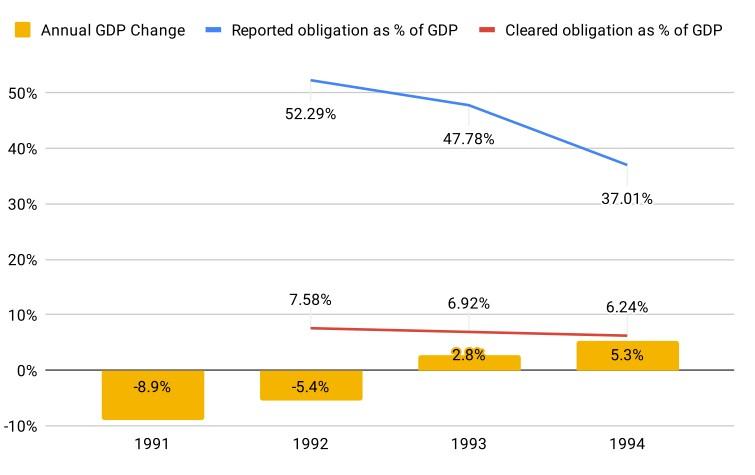

After achieving independence in 1991, Slovenia adopted multilateral set-off mechanisms to address liquidity challenges during times of economic hardship. As inflationary pressures increased and economic production declined, government authorities employed centralized payment systems to coordinate obligations among enterprises, netting outstanding debts prior to settlement.

This infrastructure, subsequently formalized through software systems known as "TETRIS," implemented liquidity-saving mechanisms to minimize the amount of capital requiring movement, enabling businesses to maintain operations despite widespread constraints on payment capabilities.

Crypto's instant settlement locks up liquidity

Rather than developing infrastructures that batch and net outstanding obligations, the majority of cryptocurrency markets have been constructed around immediate, atomic settlement, in which each individual transaction achieves finalization independently.

As a simplified example, when Alice transfers 10 ETH to Bob to complete a trade, that transfer receives full settlement onchain upon execution. Should Bob subsequently owe Alice 9 ETH from a different trade, that obligation gets processed as an independent transaction rather than being netted against the initial one. Rather than settling a net 1 ETH difference, the infrastructure processes 19 ETH worth of transfers across two separate transactions.

When aggregated across numerous trades, this design compels participants to perpetually move and pre-fund capital, even in situations where their net exposure approaches neutrality.

That means you need way more capital in the system than you otherwise would.

Buchman said

Immediate settlement eliminates counterparty risk, yet it simultaneously eliminates the capability to offset positions across a more extensive network of participants. This compression infrastructure is predominantly absent in cryptocurrency markets, which translates to more capital being necessary to sustain equivalent levels of activity.

There is a kind of ceiling on how much trade you can do, depending on how much actual assets and capital you have to meet it.

Buchman said

A lot of the firms are doing a lot of trading on credit with each other, but then when it comes time for settlement, they have to scramble for the assets.

He said

This dynamic compels cryptocurrency companies to overcollateralize their positions across exchanges and lending platforms, immobilizing capital that might otherwise be allocated to alternative uses. During times of market stress, this challenge intensifies, as firms find themselves attempting to satisfy settlement obligations while available liquidity contracts.

The missing primitive is clearing, now being rebuilt without intermediaries

Recreating clearing in its conventional format necessitates constructing a central counterparty. This structural model may create tension with an industry whose objective is replacing financial intermediaries with decentralized infrastructure.

Clearing institutions rank among the most rigorously regulated and trust-dependent organizations within finance, Buchman said. These entities absorb default risk, position themselves between participants and demand extensive coordination to operate effectively.

The cryptocurrency industry circumvented this structural model and instead fragmented the clearing function. Bilateral agreements and off-exchange settlement mechanisms introduced constrained netting capabilities, but predominantly within restricted networks built on trust relationships, leaving the fundamental problem unsolved.

Buchman and Cycles are proposing a coordination infrastructure that nets obligations among participants prior to settlement, without functioning as a central counterparty or assuming custody of participant funds.

The system's effectiveness, nevertheless, relies on widespread participation and transparency into obligations, which may prove challenging to accomplish in a fragmented marketplace where firms conduct operations across multiple venues and demonstrate reluctance to disclose exposures. In the absence of a central counterparty, the infrastructure also fails to absorb default risk, leaving participants responsible for managing counterparty exposure independently.

Orchestrating multilateral netting among independent actors may also introduce operational complexity, especially during episodes of market stress when liquidity faces existing constraints.

Buchman contends this challenge can be resolved through the application of cryptographic techniques, with obligations registered privately onchain, netted through software and validated using zero-knowledge proofs.

From this perspective, the compromise for cryptocurrency is that institutional trust gets replaced by trust in the protocol's architectural design.