BTC Volatility Reaches 8-Month Bottom: Could Bitcoin Be Poised for Major Price Movement?

While Bitcoin's volatility reaching an 8-month bottom doesn't necessarily forecast BTC's next price move, analysis of derivatives markets indicates a potential short squeeze could occur if prices surge toward $82,000.

Key takeaways:

- The implied volatility of Bitcoin has descended to a multi-month minimum, indicating trader expectations for continued price consolidation ahead.

- An overabundance of bearish sentiment among Bitcoin traders may trigger a liquidation-fueled rally pushing prices beyond the $82,000 threshold.

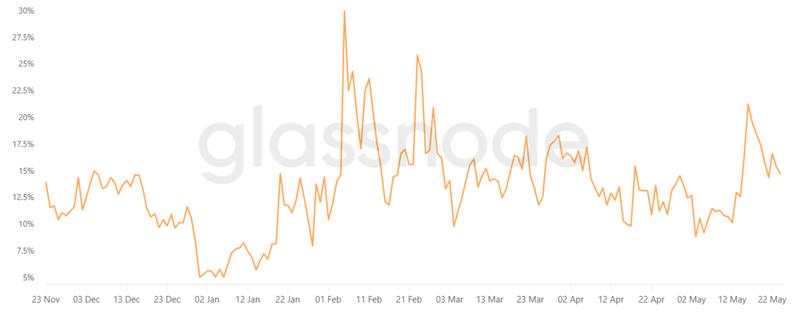

The implied volatility of Bitcoin (BTC) has fallen to 36%, marking the lowest reading witnessed in eight months and suggesting that sophisticated market participants are factoring in reduced probability of significant price fluctuations. Although diminishing volatility doesn't necessarily signal either bullish or bearish trends, analysis of Bitcoin derivatives markets points to the possibility that excessive bearish positioning could spark an upward price breakout.

During the January through February period, a rapid price drawdown triggered an initial surge in volatility levels, particularly because the decline lacked an obvious fundamental catalyst. Throughout March, despite Bitcoin maintaining a relatively confined trading range spanning $63,000 to $71,000, implied volatility remained elevated above the 50% threshold.

Market participants developed stronger conviction in the support zone around $60,000, which translated to diminished risk assessment and a corresponding decline in volatility metrics. Several market observers attribute the taming of Bitcoin price action to increased institutional market involvement and the proliferation of derivatives instruments, including the perpetual stock offerings from Strategy.

According to reports, Tyler Evans, chief investment officer of UTXO Management, indicated that digital credit instruments have established a cushion against Bitcoin's price volatility. Instead of facing pressure to liquidate their Bitcoin positions, substantial stakeholders—encompassing mining operations and corporations prioritizing Bitcoin treasury accumulation—have progressively turned to collateralized lending solutions.

Is Bitcoin volatility bound to go up?

The volatility of Bitcoin may climb back to readings exceeding 42%, considering the digital asset remains relatively immature regarding mainstream adoption and potential applications. Bitcoin's volatility has historically never sustained levels beneath 35%, though theoretically, further declines remain possible. Throughout history, substantial price movements typically materialize following periods of range-bound trading, which naturally produces decreased volatility readings.

Whether catalyzed by external developments including trade conflicts, economic intervention policies, or inflated equity market valuations, Bitcoin's price fluctuations frequently gain momentum through the forced liquidation of positions utilizing leverage.

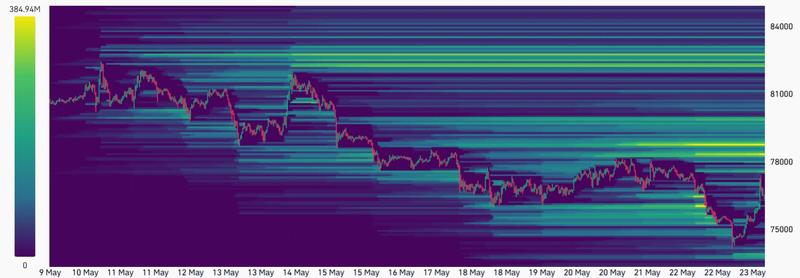

Estimates from Bitcoin liquidation heatmap analysis reveal substantial clustering of short positions (bearish bets) concentrated within the $78,000 to $83,000 price corridor. Bearish traders may have developed excessive confidence following nearly four months of Bitcoin prices remaining confined beneath the $90,000 level. Analysis of Bitcoin options skew metrics provides useful insights into the positioning strategies employed by whales and market makers.

At present, professional market participants are exhibiting concern regarding potential Bitcoin price deterioration, evidenced by put (sell) options commanding a 14% premium when compared to call (buy) contracts. During neutral market environments, this particular indicator typically fluctuates within a -6% to +6% range, yet this equilibrium has been absent throughout the preceding four-month period.

Volatility metrics alone should not serve as directional market forecasting tools. Nevertheless, considering the pessimistic sentiment prevailing within Bitcoin options trading venues, the probability exists that an upward breach above the $82,000 level would catalyze a more forceful compression of leveraged short positions, whereas a pullback testing the $72,000 support appears to be largely anticipated by market participants.