Arca Executive Warns Strategy's $15B Preferred Stock Load Has Become 'Out of Hand'

Arca's Jeff Dorman raises concerns about Strategy's capital structure, pointing to $15 billion in preferred stock liabilities and the CEO's acknowledgment of potential Bitcoin liquidations.

Increasing attention is being directed toward Strategy's preferred stock financing approach as market participants raise questions about whether its dividend payment requirements might ultimately force the firm to liquidate portions of its Bitcoin holdings.

Arca's chief investment officer Jeff Dorman stated on Thursday via an X post that the Strategy situation has now "gotten out of hand," pointing to approximately $15 billion in outstanding preferred stocks that generate roughly $1.5 billion in yearly dividend payment requirements.

According to Dorman, the financing structure could become progressively more challenging to sustain should market volatility persist, particularly with Bitcoin (BTC) currently trading approximately 16% below its year-to-date peak at around $73,737 as of this writing.

These comments contribute to an expanding conversation surrounding the sustainability of Strategy's Bitcoin-focused capital arrangement and its ability to weather extended price fluctuations without being compelled to liquidate assets.

Concerns mount over $15 billion in preferred stock

The crux of Dorman's concerns lies in Strategy's approach to financing, characterized by substantial preferred stock issuances that come with mandatory fixed dividend payments.

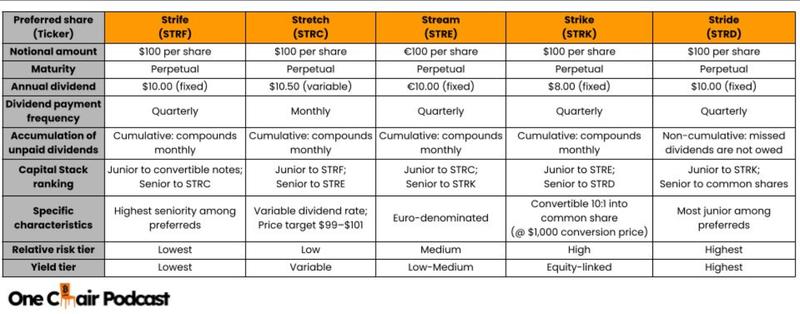

The company has brought to market five distinct preferred share classes — STRK, STRF, STRD, STRC and STRE — with each instrument featuring unique dividend structures, priority rankings and varying degrees of risk within the overall capital framework.

The financing approach, according to Dorman, was constructed under the premise that Bitcoin would experience sufficiently robust price appreciation to sustain the obligations, essentially representing a wager that BTC was "about to moon" and would generate adequate resources for future commitments.

While acknowledging that Strategy's equity capital raises provided some relief from immediate default risks, Dorman expressed confusion over the company's subsequent actions, particularly characterizing its bond repurchase decision targeting 2029 maturities as "baffling" in light of continued strain from dividend payment requirements.

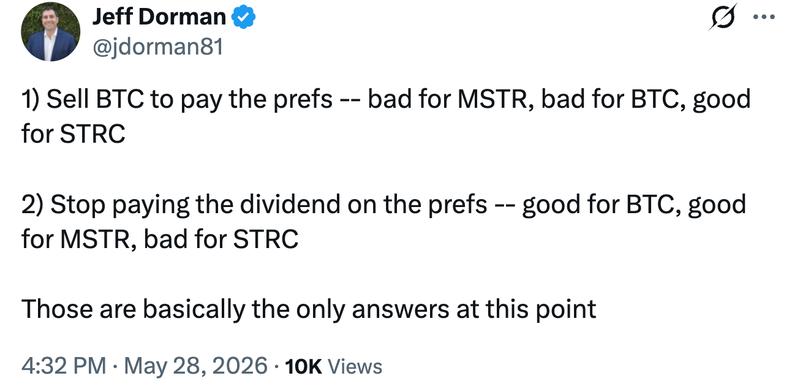

The capital structure, in Dorman's assessment, creates a situation where only severe options remain available: the company must either "sell BTC to pay the prefs" or alternatively "stop paying the dividend," with both scenarios presenting significant and disproportionate ramifications for Strategy itself, its shareholder base and the broader Bitcoin market.

Strategy CEO acknowledges potential Bitcoin liquidations as prediction market odds climb

The comments from Dorman emerged alongside confirmation from Strategy CEO Phong Le that Bitcoin sales could occur at some future date, following similar indications from Strategy executive chairman Michael Saylor who mentioned this possibility in mid-May.

"We'll likely sell Bitcoin at some point in time, but we will be net increasing our Bitcoin and more importantly, increasing our Bitcoin per share," Le stated during an exclusive appearance on CNBC Fox Business on Thursday.

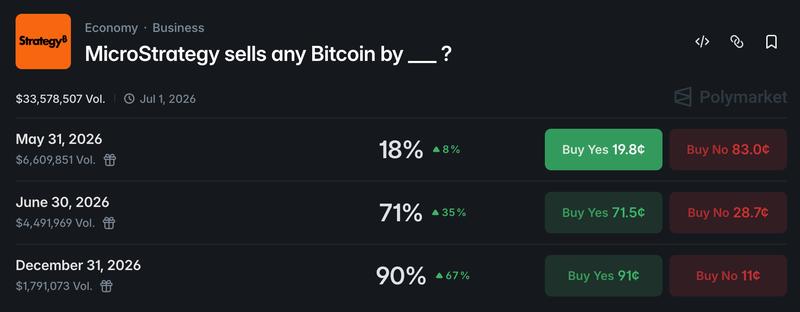

As speculation grows that Strategy may find itself needing to liquidate BTC holdings to address its balance sheet requirements and financial commitments, the decentralized prediction platform Polymarket has registered climbing probabilities for such a sale occurring throughout 2026.

Data from the "MicroStrategy sells any Bitcoin by" prediction market indicates approximately 90% probability by Dec. 31, 2026, 71% likelihood by June 30 and 18% odds by May 31.

Throughout the current year, Strategy has accumulated approximately 170,000 BTC, expanding its overall position to 843,738 BTC acquired at a combined cost of $63.87 billion and representing an average acquisition cost of about $75,700 per Bitcoin.