Why Bitcoin's funding rate remains in negative territory despite BTC climbing past $75K

Analysis reveals that forced liquidations are playing a role in Bitcoin's persistently negative funding rate, though growing institutional spot demand may provide the support needed for BTC to maintain the $75,000 threshold.

Key takeaways:

- The negative funding rates observed in Bitcoin futures markets point to bear-market liquidations and forced closures instead of indicating a fundamental change in market sentiment.

- Strong institutional capital flows into Bitcoin ETFs combined with corporate buying activity indicate that underlying spot market demand continues to hold steady.

Bitcoin (BTC) experienced a selloff during the early hours of US equity market trading, momentarily dipping beneath the $75,000 threshold before staging a recovery. The abrupt price movement resulted in $120 million worth of liquidations across leveraged long (buy) BTC futures contracts. Throughout this volatile period, the Bitcoin funding rate has continued to display negative values, a signal that may suggest additional downside potential and could provide bears with a tactical edge.

Negative funding rates have prevailed as the standard since Monday, reflecting a shortage of appetite for bullish leveraged exposure. When rates turn negative, it means short (seller) positions are the ones compensating to maintain their exposure. During typical market conditions, this metric should fluctuate within a 5% to 10% band to account for capital costs and platform risks. While a 20% rate might initially appear to demonstrate strong conviction, a deeper examination reveals additional complexity.

Forced liquidations underpin Bitcoin's negative funding rate

Most cryptocurrency exchanges compute perpetual contract funding rates at 8-hour intervals. Short-lived surges to 20%, whether positive or negative, typically don't cause significant concern among experienced traders, given they translate to roughly a 0.05% daily charge. Effectively, even when utilizing extremely high leverage such as 20x, the expense amounts to just 1%. Unless this situation extends considerably longer, it represents a minimal financial burden.

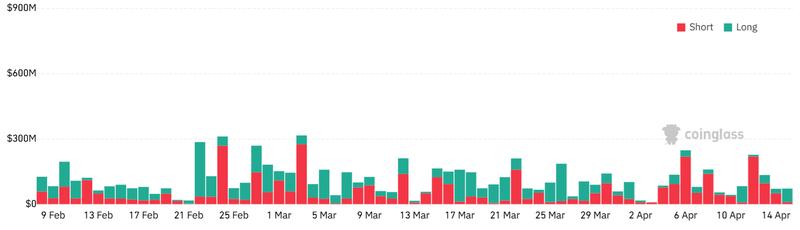

Since Monday, bearish Bitcoin positions have suffered forced liquidations totaling $365 million, which has organically depleted collateral reserves on short-side positions. Market participants may have chosen to hold their ground instead of hurrying to deposit additional margin, expecting that funding rates would naturally normalize over time. Therefore, the negative funding rate actually mirrors the losses sustained by bearish traders rather than reflecting genuine market conviction.

Throughout the past several weeks, Bitcoin's intraday price action has predominantly mirrored movements in the S&P 500 index. The US equity market surged to establish a fresh all-time high on Thursday, whereas Bitcoin continues to trade well below its $126,200 apex. Repeated attempts to reclaim and hold the $76,000 price point offer some explanation for the subdued interest observed in BTC derivatives trading venues. Nevertheless, the most recent batch of US macroeconomic releases appears favorable for risk-on assets, Bitcoin included.

According to Federal Reserve data published on Thursday, US industrial production contracted by 0.5% in March compared to the preceding month. Consumer durable goods represented the primary weak spot, with vehicle manufacturing declining 2.8%. At the same time, continuing jobless claims rose by 31,000 to reach a seasonally adjusted figure of 1.818 million for the week that concluded April 4.

Though it may seem paradoxical, the S&P 500 gained from the heightened economic recession concerns, which compelled authorities to expedite stimulus initiatives. The upward trajectory in inflation, additionally fueled by climbing oil prices, diminishes the attractiveness of maintaining fixed-income asset allocations.

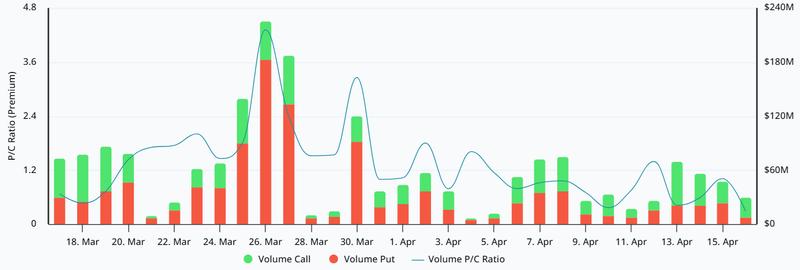

Data from the Bitcoin options marketplace shows no evidence of outsized demand for downside hedging protection. Over the previous week, the premium commanded by put (sell) options on Deribit has trailed behind that of comparable call (buy) instruments. The $921 million in aggregate net inflows directed toward US-listed Bitcoin spot ETFs across a five-day period, combined with ongoing accumulation activity from Strategy (MSTR US), has reinforced investor sentiment and confidence.

Currently, Bitcoin's negative funding rate doesn't warrant significant concern, particularly given that institutional investor appetite continues demonstrating strength within BTC's spot trading markets.