Research reveals crypto industry's near-total silence on market-maker agreements

An examination of more than 150 cryptocurrency protocols shows that less than 1% provide disclosure about their market-making deals, exposing a significant lack of transparency in token trading frameworks.

An examination of more than 150 prominent cryptocurrency protocols reveals that transparency around market-making agreements is virtually absent, even though these arrangements play a pivotal role in how tokens are traded.

The analysis, carried out by cryptocurrency advisory firm Novora, discovered that less than 1% of the examined protocols provide any disclosure regarding their terms with market makers. Throughout the entire dataset, just a single protocol—Meteora, a decentralized liquidity platform—was identified as having made public the details of its market-making agreements, according to the project's 2025 Annual Token Holder Report.

The analysis encompassed prominent sectors, including decentralized exchanges, lending platforms, perpetual futures, layer-1 and layer-2 networks, bridges and centralized exchange tokens, with protocols spanning a range from approximately $40 million to $45 billion in fully diluted valuation.

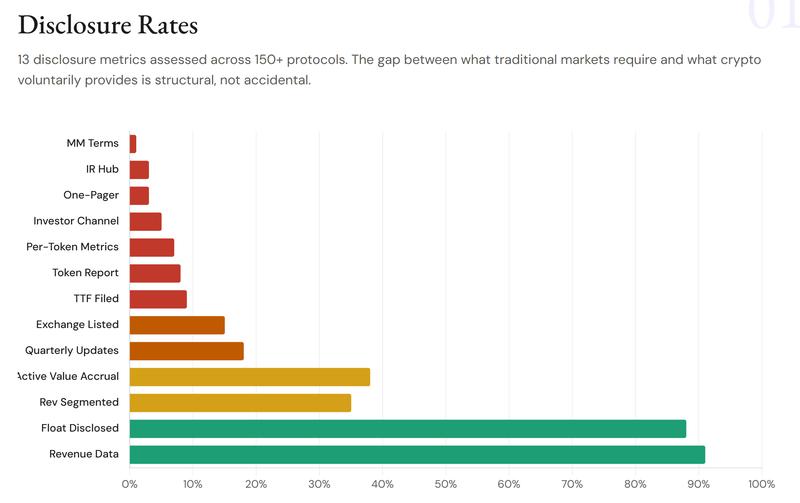

According to Novora, the protocols underwent assessment using a binary transparency framework that covered disclosure practices and third-party data coverage, with verification against public sources including Artemis, Token Terminal, Dune, DefiLlama and Blockworks Research.

"This is the single most consequential transparency gap in the industry," Novora founder Connor King wrote on X, noting that such material agreements are routinely disclosed in traditional markets. "In crypto, every market participant operates without this information," he added.

Cryptocurrency's gap in investor relations

The discovery highlights a wider investor relations (IR) deficit within the cryptocurrency space. According to Novora, 91% of the protocols under review generated revenue that could be tracked, yet only 18% released quarterly updates and a mere 8% produced token holder reports, indicating the information is available but seldom compiled into organized investor communications.

Simultaneously, third-party analytics infrastructure has reached maturity, with coverage rates surpassing 85% across leading platforms, indicating the foundational data is broadly available but infrequently formalized through official reporting channels.

Transparency varies considerably across different sectors. Perpetual futures protocols and decentralized exchanges generally perform better on disclosure and value accrual mechanisms, whereas L1 and infrastructure projects fall behind despite possessing larger market capitalizations.

Arrangements with market makers face increased examination

Lack of transparency in market-maker arrangements has historically attracted scrutiny within the crypto space, particularly concerning token loan structures that detractors argue can establish incentives to sell borrowed tokens into the market. The United States Securities and Exchange Commission (SEC) has even previously charged so-called crypto market makers with price manipulation.

As Cointelegraph reported, certain market-maker arrangements are inadequately structured and have the potential to rapidly become detrimental. One frequently employed arrangement, the "loan option model," involves projects lending tokens to market makers who subsequently deploy them for liquidity provision and trading activity, frequently connected to listing agreements.

In practical application, critics contend this structure can generate powerful incentives to sell borrowed tokens into the market, initiating price declines that benefit the market maker while leaving early-stage projects with compromised liquidity and impaired token performance.